When startup VC exits does not happen by themselves, what’s a VC to do? Exploring the topic of discussing liquidity and exit strategy at term sheet level.

First article leading up to the upcoming Dune Venture Days in Dubai.

The Exit Gap in Most VC Markets

Across MENA, Africa, and Europe, venture capital ecosystems share a common challenge: the path to liquidity remains uncertain, unpredictable, and often an afterthought. In MENA, startups have raised over $11 billion since 2021, yet fewer than 7.5% have achieved exits. Africa recorded only 26 venture-backed exits in 2024, returning just $0.13 per invested dollar. European secondary markets, while more developed, still leave many GPs scrambling when fund lifecycles demand returns.

The numbers tell a challenging story. The VC markets across MENA, Africa and Europe are all maturing, evolving, even booming in the case of MENA. Deals are happening, new funds are being set up, but…….. everyone is also waiting on liquidity and DPI.

This raises a fundamental question: Should exit thinking be embedded directly into the term sheet itself?, or more precisely, how should liquidity strategy be presented in your term sheet?

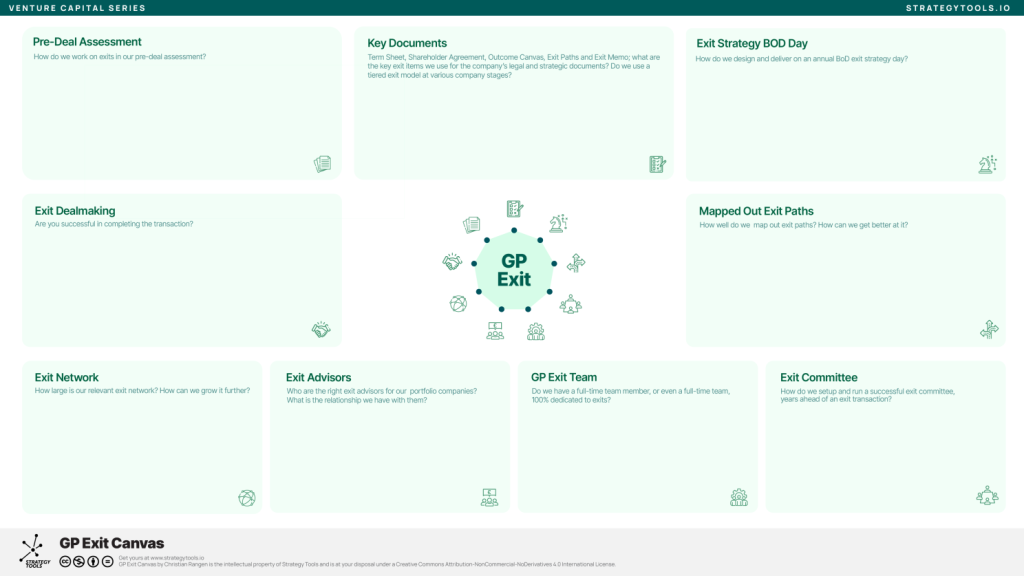

The GP Exit Canvas: A Framework for Strategic Exit Planning

The GP Exit Canvas, developed through extensive work with fund managers across global VC markets, provides a structured visual framework for integrating exit strategy thinking from day one of the investment process. It consists of nine interconnected building blocks:

Building Block

- Pre-Deal Assessment

How do we work on exits in our pre-deal assessment?

2. Key Documents

What exit items do we use in term sheets, shareholder agreements, and exit memos?

3. Exit Strategy BOD Day

How do we design and deliver an annual board exit strategy day?

4. Mapped Out Exit Paths

How well do we map out exit paths for each portfolio company?

5. Exit Committee

How do we setup and run an exit committee years ahead of a transaction?

6. GP Exit Team

Do we have team members dedicated to exits?

7. Exit Advisors

Who are the right exit advisors for our portfolio companies?

8. Exit Network

How large is our relevant exit network and how can we grow it?

9. Exit Dealmaking

Are we successful in completing exit transactions?

Notice that “Key Documents” sits prominently in this framework. The canvas explicitly asks: What are the key exit items we use for the company’s legal and strategic documents? Do we use a tiered exit model at various company stages? This is where the term sheet becomes a critical tool for exit planning.

The VC Debate: Should Term Sheets Include Exit Provisions?

The question of whether to include explicit liquidity and exit provisions in term sheets divides opinion among fund managers. Let’s examine both sides.

The Case Against

Premature constraints on founder optionality. Critics argue that embedding exit timelines into term sheets creates rigid structures that may not serve the company’s best interests. Markets shift, opportunities emerge unexpectedly, and what looks like the right exit path at Series A may be completely wrong by Series C. Founders need flexibility to pursue the best outcomes, not contractual obligations that force premature decisions.

Potential misalignment with founder vision. Some founders view explicit exit provisions as a signal that investors are more focused on their own returns than building a truly transformative company. This can create tension from day one and may deter founders who are building for the long term.

Negotiation complexity. Adding detailed exit provisions increases the complexity of term sheet negotiations, potentially slowing deal velocity and adding legal costs at a stage where founders often have limited resources.

The Case For

Alignment from day one. Proponents argue that discussing exit paths early actually creates better alignment between founders and investors. When both parties understand and agree on potential liquidity scenarios, there are fewer surprises later. As the GP Exit Canvas emphasizes, exit planning isn’t separate from investment strategy—it is investment strategy.

LP pressure demands clarity. Limited Partners are increasingly demanding DPI (distributions to paid-in capital) rather than just paper returns. In markets like MENA and Africa, where exits are scarce, LPs want to see evidence that GPs have thought through liquidity paths before committing capital. Having exit provisions in term sheets signals sophistication and planning.

Structuring for market realities. In regions with underdeveloped IPO markets and fewer strategic acquirers, secondary sales and tiered liquidity models often represent the most realistic path to returns. Building these mechanisms into deal structures from the start ensures they can be executed when opportunities arise.

Creating exit-ready documentation. When exit opportunities emerge, deals often fail because documentation isn’t ready for institutional buyer due diligence. Term sheets that anticipate exit requirements—drag-along rights, tag-along protections, information rights—create companies that can move quickly when windows open.

The Verdict: Yes, With Nuance

The evidence is clear: paths and timelines to liquidity are key for VCs and should be covered in term sheets. However, this doesn’t mean imposing rigid exit schedules or forcing founders into narrow outcomes. Instead, it means creating flexible frameworks that acknowledge the importance of liquidity while preserving optionality.

The most successful VCs think backward from liquidity events when making investment decisions. As the GP Exit Canvas demonstrates, this backward-thinking approach should be embedded in every aspect of the investment process, including the foundational document that governs the investor-founder relationship.

For emerging market funds, where smaller pools of potential acquirers and less developed exit markets create additional challenges, the discipline of incorporating exit thinking into term sheets can mean the difference between a successful fund and one that struggles to return capital to LPs.

Three Liquidity Mechanisms: Sample Term Sheet Language

Below are three examples of different liquidity mechanisms that can be incorporated into term sheets, each suited to different investment contexts and portfolio company stages.

1. Strategic Acquisition Facilitation Clause

Context: Appropriate for early-stage investments where strategic M&A is the most likely exit path, particularly in sectors with active corporate acquirers (fintech, healthtech, agritech).

SAMPLE TERM SHEET LANGUAGE

Exit Strategy Facilitation

Strategic Exit Support: Upon the Company achieving annual recurring revenue of [USD 2,000,000] or cumulative revenue of [USD 5,000,000], the Investors shall actively facilitate introductions to potential strategic acquirers identified in the pre-investment Exit Path Assessment. The Company shall maintain an updated list of no fewer than fifty (50) potential strategic acquirers, reviewed and updated at each Board Exit Strategy Day.

Exit Readiness Milestones: The Company agrees to achieve “exit-ready” status within thirty-six (36) months of closing, including: (a) completion of SOC 2 Type II certification or equivalent, (b) audited financial statements prepared in accordance with IFRS, (c) documented regulatory approvals and compliance records, and (d) clean cap table with all option grants properly documented.

Drag-Along Rights: In the event of a bona fide acquisition offer valued at or above [3x] the post-money valuation of this round, approved by (i) a majority of the Board of Directors and (ii) holders of a majority of the Preferred Stock, all shareholders shall be required to participate in such transaction on the same terms and conditions.

Information Rights for Exit: The Company shall provide Investors with monthly operating metrics in a format suitable for potential acquirer due diligence, and shall grant Investors reasonable access to management for the purpose of facilitating strategic discussions with potential acquirers, subject to appropriate confidentiality protections.

2. Tiered Liquidity Model (1/3, 1/3, 1/3 Structure)

Context: Designed for growth-stage investments where the investor seeks to manage risk and generate early DPI while maintaining upside exposure. Particularly relevant in MENA and Africa where full exits are rare but secondary markets are developing.

SAMPLE TERM SHEET LANGUAGE

Tiered Liquidity Structure

Liquidity Schedule: The Investors’ shareholding shall be subject to the following tiered liquidity framework, designed to balance early returns with continued participation in Company growth:

Tranche 1 – Series B Secondary (One-Third of Position): Upon completion of the Company’s Series B financing round at a pre-money valuation of at least [3x] the post-money valuation of this round, the Investors shall have the right (but not the obligation) to sell up to one-third (33.33%) of their shareholding to incoming investors or approved secondary buyers. The Company shall use commercially reasonable efforts to facilitate such secondary sale as part of the Series B transaction, including allocating reasonable capacity in the round for secondary purchases and providing necessary documentation and representations.

Tranche 2 – Pre-IPO/Series D Secondary (One-Third of Position): Upon completion of a Series D financing round or a pre-IPO financing round at a pre-money valuation of at least [8x] the post-money valuation of this round, the Investors shall have the right to sell an additional one-third (33.33%) of their original shareholding (or 50% of remaining position) through secondary sale mechanisms. The Company agrees to include standard secondary sale provisions in its Series D or pre-IPO documentation, and shall not unreasonably withhold consent to transfers to qualified institutional buyers.

Tranche 3 – Ultimate Exit/IPO (Remaining Position): The Investors’ remaining shareholding (one-third of original position) shall be held until the Company’s ultimate liquidity event, whether through IPO, strategic acquisition, or other qualifying exit transaction. In the event of an IPO, the Investors agree to customary lock-up provisions not exceeding one hundred eighty (180) days, following which they may dispose of shares at their discretion.

Valuation Floor Protection: The secondary sale rights described in Tranches 1 and 2 above shall only be exercisable if the applicable round valuation represents at least a [2.5x] multiple on the Investor’s cost basis for Tranche 1, and a [5x] multiple for Tranche 2. If such thresholds are not met, the secondary rights shall roll forward to the next qualifying financing round.

Company Facilitation Obligation: The Company shall designate a member of senior management responsible for coordinating secondary sale processes and maintaining relationships with secondary market platforms and qualified buyers. The Company shall not impose transfer restrictions or exercise rights of first refusal in a manner designed to frustrate the Investors’ exercise of the rights described herein.

3. Redemption and Put Option Mechanism

Context: Appropriate for later-stage investments or situations where market exit uncertainty is high, providing investors with a guaranteed liquidity path while giving the Company flexibility on timing.

SAMPLE TERM SHEET LANGUAGE

Redemption and Put Option Rights

Redemption Right: Commencing on the sixth (6th) anniversary of the closing date (“Redemption Date”), and upon written request from holders of at least a majority of the then-outstanding Preferred Stock, the Company shall redeem the Preferred Stock in three (3) equal annual installments at a price per share equal to the greater of: (a) the original purchase price plus any accrued but unpaid dividends, or (b) the fair market value as determined by an independent valuation conducted by a mutually agreed third-party valuation firm.

Put Option: In the event that no qualifying liquidity event (defined as an IPO, strategic acquisition, or secondary sale opportunity at or above [2x] the original purchase price) has occurred by the fifth (5th) anniversary of closing, the Investors shall have the right to require the Company to facilitate a sale of the Investors’ shares to (i) existing shareholders, (ii) the Company (subject to legal restrictions), or (iii) third-party buyers identified by the Company, at a price equal to the higher of (a) [1.5x] the original purchase price or (b) fair market value as determined by independent valuation.

Company Call Option: The Company shall have the right, but not the obligation, to call and repurchase the Investors’ shares at any time after the fourth (4th) anniversary at a price equal to the higher of (a) [2.5x] the original purchase price or (b) fair market value. This call option shall expire upon the occurrence of a qualifying liquidity event.

Exit Window Coordination: The Company agrees to engage an investment bank or M&A advisor to conduct a formal market assessment of exit opportunities no later than the fourth (4th) anniversary of closing, with the results of such assessment to be shared with the Board of Directors and used to inform liquidity planning discussions.

Implementing Exit Thinking: Practical Steps for GPs

The GP Exit Canvas provides a comprehensive framework for making exit planning systematic rather than sporadic. When implementing exit provisions in term sheets, consider these principles:

Start the conversation early. Use the pre-deal assessment phase to discuss exit scenarios openly with founders. This conversation will inform which term sheet provisions are most appropriate and help identify potential misalignment before it becomes a problem.

Match provisions to context. A fintech startup with clear strategic acquirer interest needs different provisions than a B2B SaaS company targeting eventual IPO. The three examples above illustrate this range—use them as starting points, not templates.

Build in flexibility. The best exit provisions create optionality rather than obligation. Rights to sell don’t mean requirements to sell. Valuation floors protect against fire sales while preserving upside.

Integrate with governance. Exit provisions in term sheets should connect to ongoing governance mechanisms—annual Exit Strategy Board Days, exit committees, and regular exit readiness assessments as outlined in the GP Exit Canvas.

Communicate with LPs. When raising your next fund, point to these term sheet provisions as evidence of your systematic approach to liquidity. LPs increasingly want to see DPI, and demonstrating that you’ve built exit thinking into your investment process from day one differentiates you from GPs who treat exits as an afterthought.

Conclusion

In venture capital, capabilities compound over time into competitive advantages. Funds that embed exit thinking into their term sheets—and across all nine elements of the GP Exit Canvas—build a systematic capability that serves portfolio companies, LPs, and their own track records.

For fund managers operating in MENA, Africa, and Europe, where exit markets remain challenging but opportunities are growing, this systematic approach isn’t optional—it’s essential. The term sheet is where that discipline starts.

The most successful venture capital firms don’t just pick winners; they systematically create the conditions for winning exits. Make your term sheet part of that system.

_______________

About Dune Venture Days: Welcome to the first edition of DUNE Venture Days: a complimentary, invite-only venture capital gathering designed for a curated group of VCs, startup investors, and ecosystem leaders. DUNE will take place in partnership with Dubai CommerCity and alongside the WORLDEF Dubai 2026 Conference.

DUNE is 100% complimentary. It is simply about giving back to the VC ecosystem — a moment to strengthen existing relationships, build new ones, and bring together people we genuinely enjoy exchanging ideas with. Apply to join at Dune Venture Days.

About the GP Exit Canvas: The GP Exit Canvas is part of the Venture Capital Series developed by Strategy Tools. Download the canvas and explore additional resources at www.strategytools.io.

About the Author: Christian Rangen is a strategy advisor and business school faculty member who works with VC/PE firms, fund-of-funds, DFIs, and governments on venture capital ecosystem development. He delivers VC Masterclasses and mentors fund managers globally.