Just flying back from a week with founders in Dubai, one of the most common questions we received, “what should I put in my pitch deck?”.

Our answer: “you are asking the wrong question. You need to develop all six decks”

By: Christian Rangen, global advisor to VCs, FoF’s & ecosystem builders. Faculty, advisor, investor Sanjana Raheja, advisor to early-stage founders, accelerators, & innovation programs

Don’t bring the wrong tool for the job

Over the last 15 years we have worked with 1000’s of founders on investor readiness and fundraising. Pre-seed health tech, post-IPO energy tech and everything in between. One constant: the pitch deck. Yet, in our experience, this is only a small fraction of the story. Our experience; you really need six different decks.

Too often, we have seen founders send out their pitch deck (which is not designed to be sent out), and equally often we have seen founders try to cramp 21 slides into a 30. Min first meeting call (when a 6-slide meeting deck would have sufficed). Most founders, maybe even 90%, bring the wrong tool for the job. As a founder, make sure you have the right toolkit available to you. In our experience. That means six unique investor decks, each serving its own purpose, each perfect for its own job.

Understand the investors you will meet

As a founder, you can expect to meet three categories of investors. It’s useful to keep this in mind as you build your decks and fundraising process.

Lead

A lead investor will set the terms, set the valuation, give you a term sheet, do the due diligence, structure the round, (often) bring in the co-investors.

In many cases, a lead investor will also set up a 20% ESOP (pre-round), require you to incorporate in places like Delaware and reshuffle management.

These investors care about your decks, but they care far more about your data room, the 20+ customer interviews they are going to do, the legal, team, market and technical due diligence tracks they will run and ultimately the totality of the investment case.

Qualified

A qualified investor understands all the points and work listed above, but does not have the time, bandwidth or size of investment here where they would commit to doing this work. Instead, for the moment, they are happy to take a smaller slice, what we might call a listing post; but might step into a lead investor role in a future round.

A qualified investor might have access to your data room, financial models and years of financial statements, but they are unlikely to spend much time on it. They rely on you, the founding team, the board and often the (even more qualified) lead investors to handle the work that comes with the round. But, they do care about your decks, as this is likely the only documents they will spend significant time on.

Unqualified

An unqualified investor is likely going to be a friend, family, high-net worth or business angel. They are mostly highly competent people, but with limited time and experience with early-stage investment. Often, they would not know how to truly assess a startup, and rely largely on trust and relationships to commit to the deal.

For this group, the pitch deck or full deck is likely the only thing they will actually read. They might have questions, but will usually get these answers from the founders or fellow co-investors, unlikely to ever dig deeply into the case.

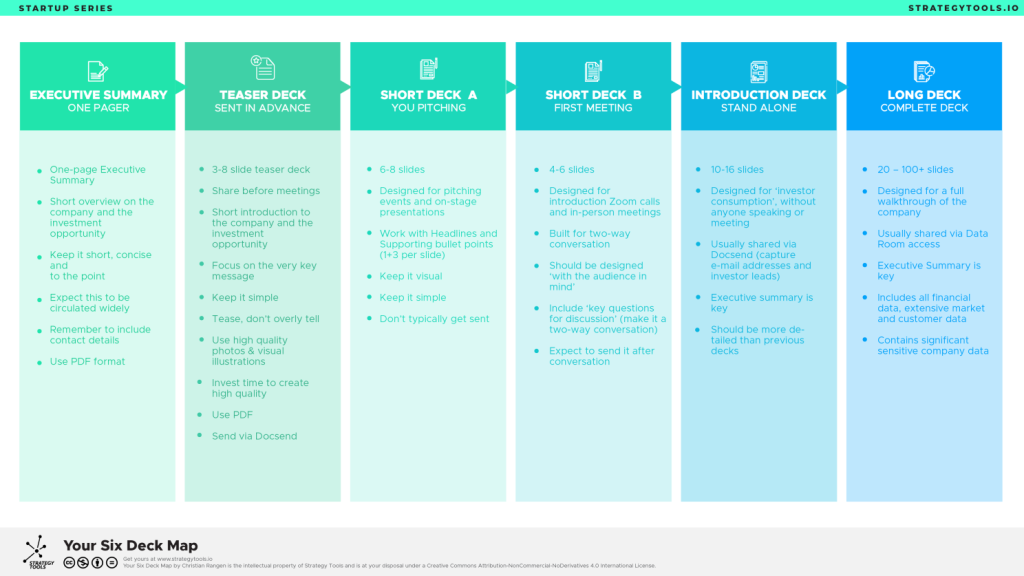

The six decks you need

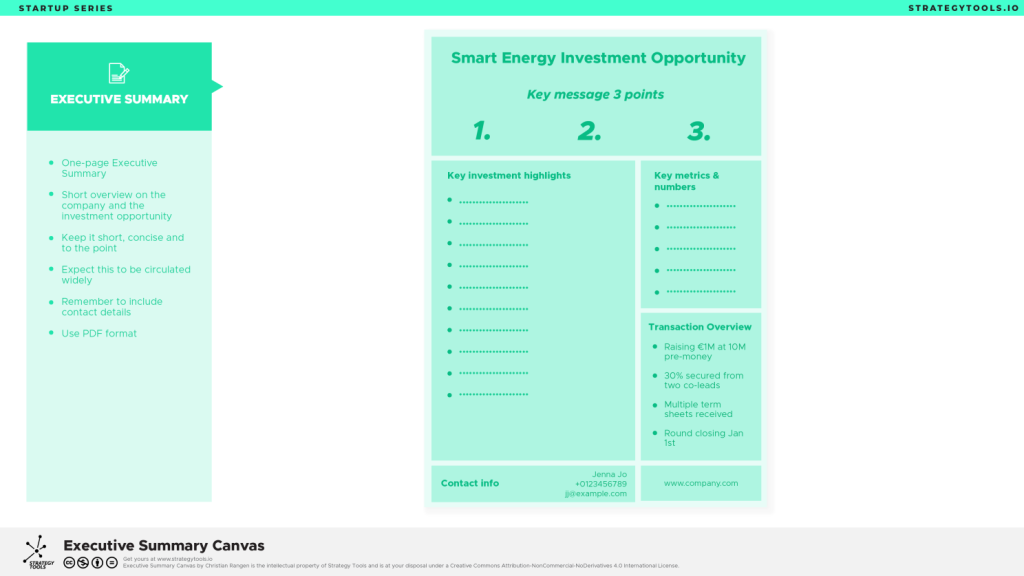

1. Executive Summary

Purpose: A strong one-pager that can be widely shared by e-mail

Format: 1-page

Content: High-level overview

Most common mistake founders do: putting in too much information

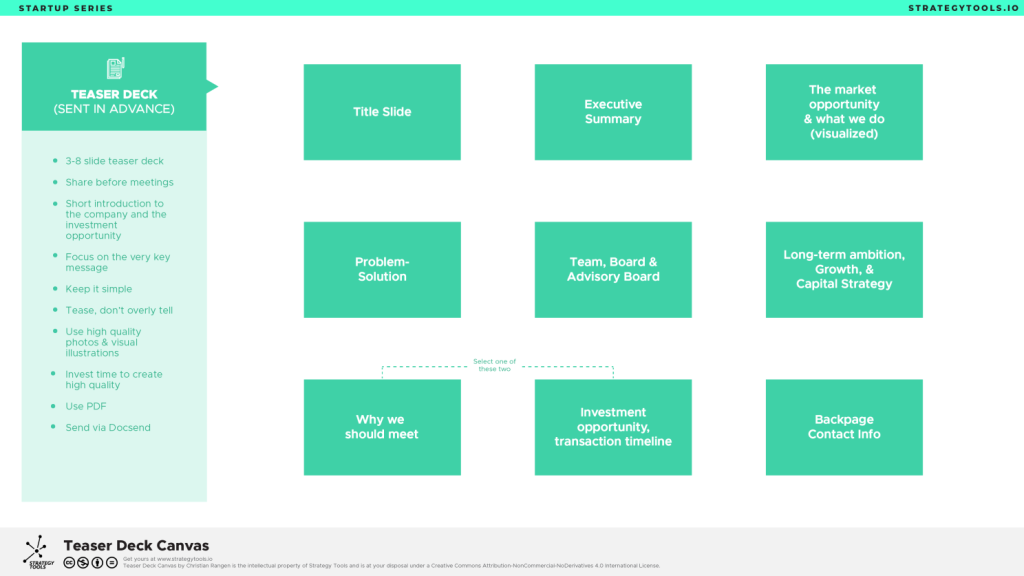

2. Teaser Deck

Purpose: A visually strong deck to be shared in advance of the first meeting

Format: 3-8-slides. Send in PDF or via Docsend

Content: Teasing investors on the 3-5 key points on the deal.

Most common mistake founders do: Sharing too much information. Not including a timeline and structure on the round

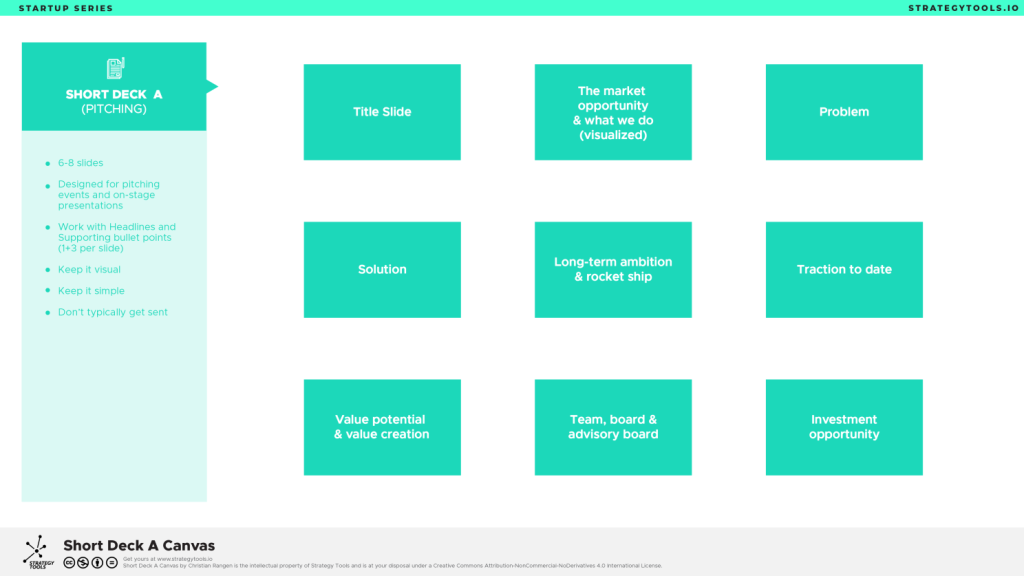

3. Short deck A: Your pitch deck

Purpose: The traditional ‘pitch deck’. But beware, this is designed to always have you in the room, giving a voice over. Removing you from the deck often leave it missing vital information.

Format: 6-8 slides. Use for pitches, not for sending out

Content: A visual story to support a founder pitching live on a stage or online

Most common mistake founders do: Three; – Cramming in too much information – Not having a ‘how to invest slide’ (Deal structure, deal timeline, committed investors, timeline to close and how to invest) – Sending it out, when the founder is not doing voice over. 90% of the time, you are better off sending deck 5. Introduction instead.

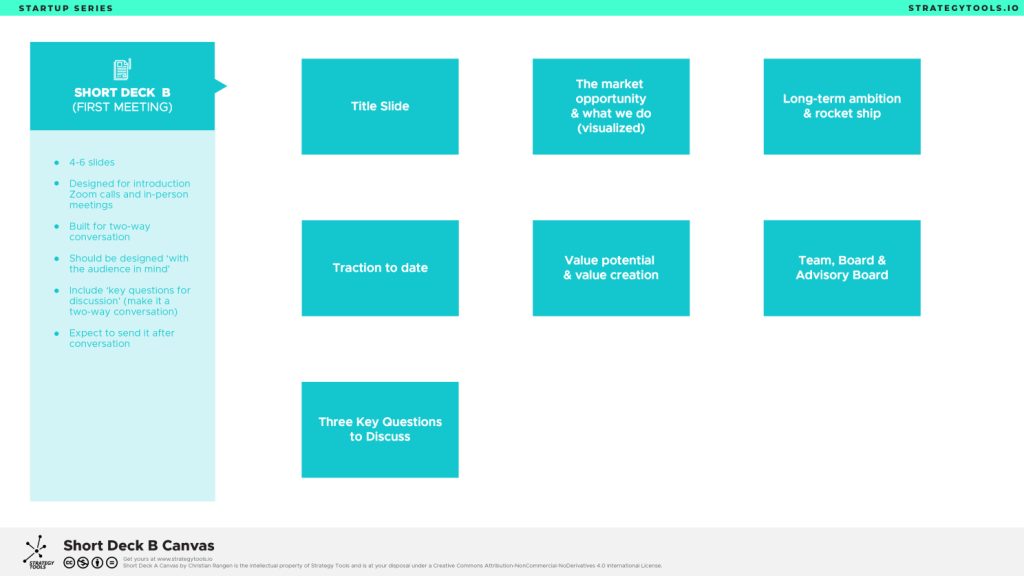

4. Short deck B: First meeting deck

Purpose: A short and concise deck for your first meeting. Design it for few slides + key questions you ask so you can steer the conversation.

Format: 4-6 slides, last slide should always contain ‘three questions’. Keep all other slides in the appendix as needed.

Content: Overview on the deal, designed to get a good, two-way conversation started

Most common mistake founders do: Too many slides, no questions to ask. As a consequence, it becomes a ‘too much information pitch meeting’. No good.

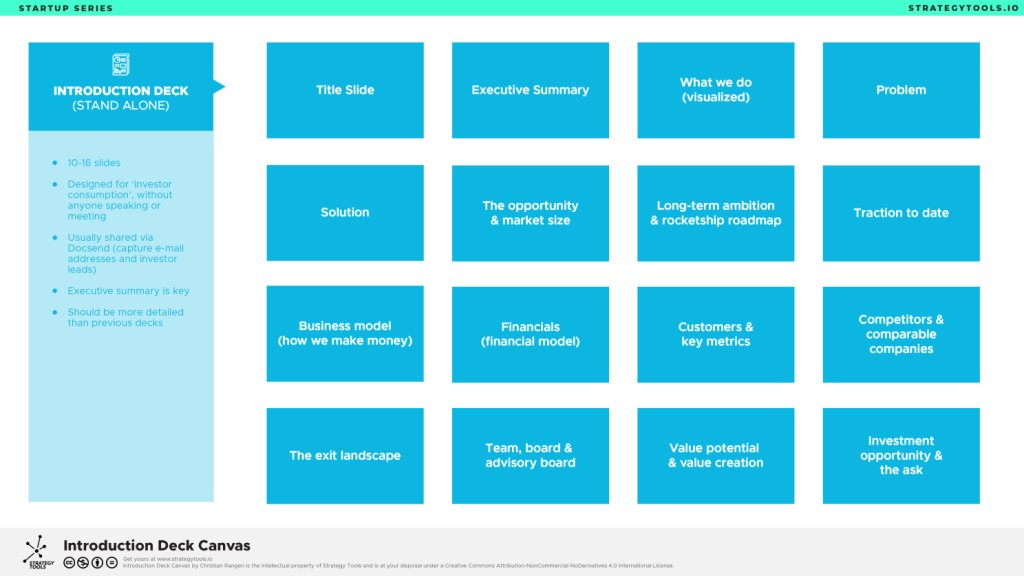

5. Introduction deck: Investment teaser

Purpose: The main deck, designed to be read by investors without you in the room

Format: 10-16 (can go to 20) slides. Send via PDF or share via Docsend

Content: A solid walk through of the business, the future ambitions and the deal terms

Most common mistake founders do: Not putting in an executive summary as slide #2, just after the frontpag

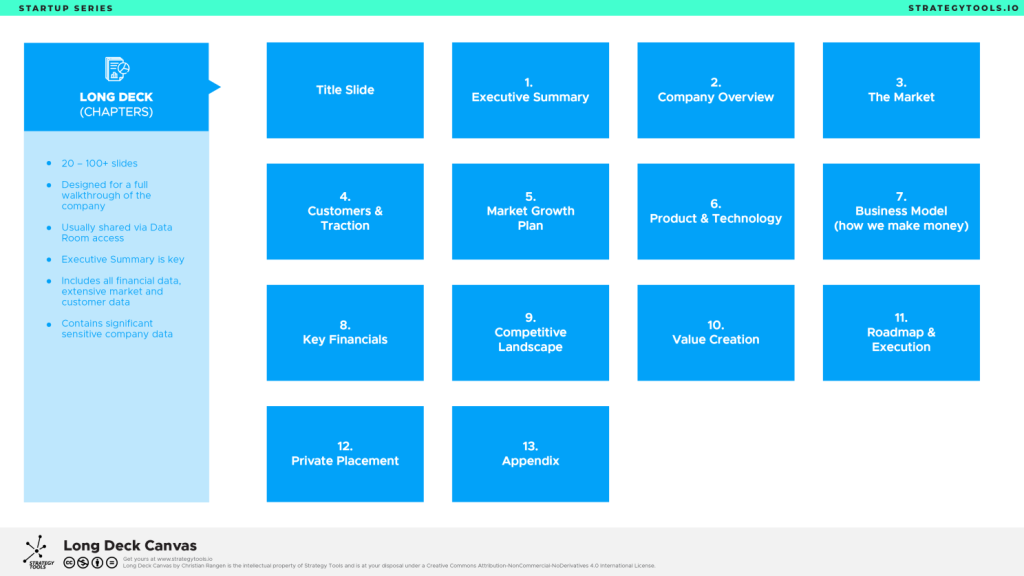

6. Long deck: Investment proposal

Purpose: This is your extensive, sharing all sensitive detail-deck. This deck is designed to give your investors an honest, detailed analysis of the company and the investment case

Format: 20-100+ slides, regularly 50-60 slides. Only shared to most serious investors, maybe after the first 3-4 meetings

Content: An extensive, incredibly detailed analysis of the business, investment case and future potential.

Most common mistake founders do: Not using an executive summary, not having enough depth on numbers and financials, not including anything on investor liquidity and exit strategy

Time to go to work

Six decks; different purposes. Do not be overwhelmed. These decks are all built on the same platform, your future success narrative. All you need to do is package them for the readers. The number one mistake, not selecting the right deck for the right purpose.

Good luck!

This article is part of the Startup Series at Strategy Tools, helping founders, investors, and ecosystem builders across MENA navigate the journey from startup to scale-up. Read more about Scale Up MENA here.