By: Christian Rangen & Rick Rasmussen

Over the past 15+ years of working with startup ecosystems across the globe, we’ve watched countless founders make the same expensive mistakes. They give away too much equity too early. They accept SAFE terms they don’t understand. They reach Series B only to discover their ownership has been diluted to single digits.

It doesn’t have to be this way.

The good news? Entrepreneurial finance isn’t rocket science. With the right readings, you can understand the mechanics of dilution, the vocabulary of venture deals, and the strategic choices that protect your ownership over multiple rounds.

We’ve curated this reading list based on three criteria: practical applicability, clarity of explanation, and relevance to the current fundraising environment. Whether you’re splitting equity with co-founders or negotiating your Series B, these books will give you the knowledge to make informed decisions.

We also cover this material in-depth in our Scale Up! Masterclasses. Want the short summary? Start with the Scaling Up in MENA story.

Why This Reading List Matters

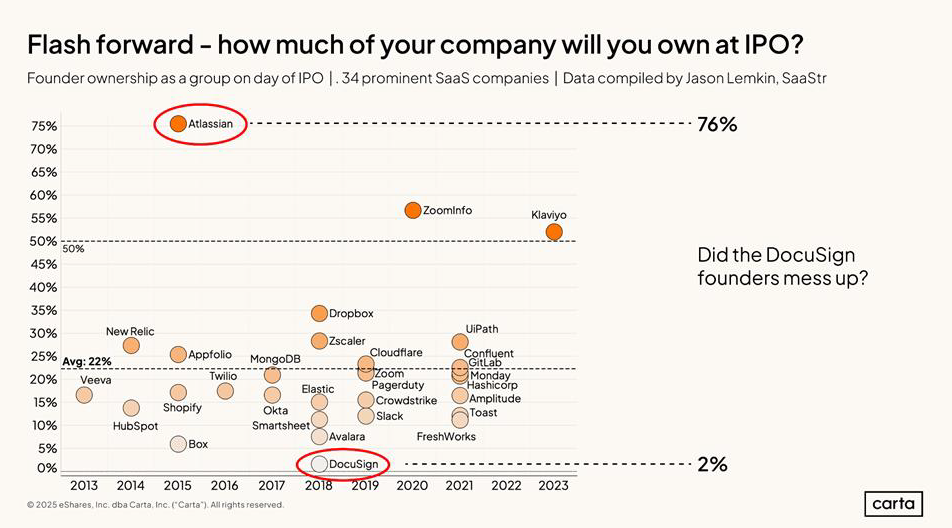

According to recent Carta data analyzing over 43,000 US startups, the median founding team owns just 56% of their company after their seed round. By Series A, that drops to 36%. By Series B, founders collectively own just 23% of the company they built.

Think about that. Less than four years after incorporation, the founding team typically owns less than a quarter of their company.

Some dilution is inevitable—you need capital to grow. But we’ve seen too many founders accept unnecessary dilution simply because they didn’t understand their options. The difference between a founder who owns 8% at exit versus 15% can mean millions of dollars and fundamentally different life outcomes.

These ten books represent your education in avoiding those costly mistakes.

The Reading List: From Foundation to Mastery

Tier 1: Essential Foundation (Start Here)

1. Foundational Equity (Carta, 2025)

Start here. Not with a paid book, but with Carta’s free 52-page report on foundational equity.

This document contains the most current data on equity splits, dilution patterns, and fundraising benchmarks. You’ll learn that 46% of two-founder teams now split equity equally (up from 32% in 2017), that solo-founded startups have increased from 17% to 35% of all new companies, and that approximately 24% of two-founder teams lose a co-founder by year four.

The data is current (through Q1 2025), comprehensive, and directly applicable to decisions you’ll face in the next 90 days.

Key insight: The report shows that SAFE valuation caps increased significantly in Q1 2025 for rounds above $500K, but the median seed round valuation remains at approximately $14-16M. This helps you calibrate your expectations against market reality.

2. Slicing Pie: Funding Your Company Without Funds (Mike Moyer)

Before you raise a dollar, you need to split equity with co-founders fairly. This is where most founding teams start with anxiety and emotion rather than frameworks.

Moyer’s “Slicing Pie” method provides a dynamic equity split model based on relative contributions over time. While controversial in some circles (critics argue it’s complex to administer), the underlying principle is valuable: equity should reflect actual contributions, not just initial promises.

The book is particularly useful for pre-seed teams trying to figure out fair splits when one founder contributes capital, another contributes code, and a third contributes customer relationships.

Moyer has written two companion books that are both worth reading, Slicing Pie Handbook goes into more depth on other who contribute to the company (suppliers, landlords, creditors) and Will Work for Pie covers issues including fair pay and advanced pie slicing skills.

When to read it: Before you sign your founder equity agreements. Many founders rush this step, creating resentment that festers for years.

3. Founder’s Pocket Guide: Cap Tables (Stephen R. Poland)

At just 100 pages, this is the most accessible introduction to capitalization tables available. Poland explains what a cap table is, how to read one, and—critically—how to model what happens to your ownership through multiple funding rounds.

The book covers basics like fully diluted ownership, option pools, and liquidation preferences in language that doesn’t require a finance degree.

Key insight: Most founders don’t realize that the option pool typically comes out of founder shares, not investor shares. This means if you agree to a 15% option pool as part of your Series A, your dilution is higher than you might expect. Poland explains this clearly with examples.

4. All of the other books in the Founder’s Pocket Guide Series:

Convertible Debt Founder Equity Splits Friends and Family Funding Raising Angel Capital Startup Valuation Stock Options and Equity Compensation Term Sheets and Preferred Shares

Each of these are focused on the circumstances you may be facing during your early raise. This is the companion volume to the cap table guide, focused specifically on understanding term sheets.

Steven R. Poland and co-authors break down each one of these topics in easy-to-read tomes of under 100 pages apiece. Most importantly, he explains what matters and in what scenarios they may significantly impact your outcomes.

When to read them: When you start to run into situations that involve other parties that may be looking to invest or will affect your cap table. Don’t sign anything until you’ve read these books and understand every clause.

One Key insight: A $20M post-money valuation with a 1x non-participating liquidation preference is often better for founders than a $25M valuation with a 1.5x participating preference. Term Sheets and Preferred Shares teaches you to see beyond the headline number.

5. Venture Deals: Be Smarter Than Your Lawyer and Venture Capitalist (Brad Feld & Jason Mendelson)

This is the definitive guide to understanding venture capital term sheets and negotiations. Feld and Mendelson (both experienced VCs) pull back the curtain on how VCs think about deal terms, what they care about most, and where founders have negotiating leverage.

The book is comprehensive (around 300 pages) but very readable. It covers everything from economics (valuation, option pool, liquidation preferences) to control (board composition, protective provisions) to other terms (drag-along, right of first refusal, redemption rights).

What makes this book exceptional is the VC perspective. Feld and Mendelson explain why VCs ask for certain terms and which terms matter most to them. This helps you understand where to spend your negotiating capital.

Current relevance: The book is regularly updated. Make sure you get the 5th edition (2024) which reflects current market practices around SAFEs, rolling funds, and other recent innovations.

Tier 3: Strategic Depth

6. Entrepreneurial Finance: The Art and Science of Growing Ventures (Alemany & Andreoli)

This is a proper textbook used in entrepreneurial finance courses at top business schools, including LBS. It’s a great introduction text, covering everything from valuation to financial strategies to basic instruments.

The book provides frameworks for thinking about financial strategy in the European context, with a clear goal to fill a gap in the European market.

When to read it: After you’ve raised your pre-seed round and want to think more strategically about financial planning for later stages.

7. Fundamentals of Entrepreneurial Finance (Hellmann & Da Rin)

Another academic text, but with a more modern, streamlined approach than traditional finance textbooks. Hellmann and Da Rin focus specifically on the unique aspects of financing entrepreneurial ventures versus established companies.

The book covers topics like convertible notes, SAFEs, venture debt, and the relationship between financing choices and business model development. It’s particularly strong on helping you understand why different financing instruments exist and when each is appropriate.

Key strength: The book includes numerous case studies from real companies, helping you see how financial decisions play out in practice.

Tier 4: Comprehensive References

8. The Holloway Guide to Raising Venture Capital (Andy Sparks, et al.)

This isn’t a traditional book—it’s a comprehensive, regularly updated online guide (though available in print). The Holloway Guide is essentially an encyclopedia of venture capital fundraising.

The guide covers everything: how to find investors, craft your pitch, negotiate terms, conduct due diligence, close the round, and manage investor relationships post-funding. It includes templates, checklists, and current market data.

What makes it special: The guide is continuously updated to reflect current market conditions. The section on SAFEs, for example, includes the most current data on valuation caps, discount rates, and conversion mechanics.

When to use it: As a reference throughout your fundraising journey. You won’t read it cover-to-cover, but you’ll return to specific sections repeatedly as you encounter new situations.

9. Startup Law and Fundraising (Swegle)

When the person on the other side of the table is an attorney trained in securities law or hires someone with that background, this book (subtitled “for entrepreneurs and startup advisors”) can provide context and background to help you parse and work your way through the legal morass.

Weighing in over 500 pages, the seventeen chapters are well organized, starting with Overview of Legal and Regulatory Mistakes, through Intellectual Property, Securities Laws, Fundraising and Exit, this book should be a staple for any semi-legal-minded founder that is looking to learn, avoid issues and have the best possible outcomes.

10. Venture Capital Deal Terms: A Guide to Negotiating and Structuring Venture Capital Transactions (de Vries, et.al.)

Written by a VC and two lawyers, this book unpacks deal terms and legal structures easily.

The book is packed and quite extensive. But when you’re negotiating specific terms and need to understand the legal implications, this is the definitive resource.

Who should read it: Founders negotiating Series B or later rounds, or anyone who wants deep understanding of the legal mechanics of venture deals.

How to Use This Reading List

Don’t try to read all ten books before you start fundraising. Here’s a more practical approach:

Pre-fundraising (Before incorporation):

- Read Slicing Pie for co-founder equity splits

- Read Founder’s Pocket Guide: Cap Tables to understand the basics

- Read Scaling up in MENA

First fundraising round (Pre-seed/Seed):

- Read Foundational Equity (Carta) for current market data

- Read Founder’s Pocket Guide: Term Sheets before reviewing any terms

- Read Venture Deals when you’re actively negotiating

Post-seed (Planning for Series A):

- Read Founder’s Pocket Guide: Startup Valuation

- Read Entrepreneurial Finance for strategic planning

- Use The Holloway Guide as a reference

Series A and beyond:

- Read Fundamentals of Entrepreneurial Finance for depth

- Keep Venture Capital Deal Terms as a reference

- Return to Foundational Equity annually for updated market data

Three Critical Insights From This Reading List

After absorbing these resources, three insights emerge that every founder should internalize:

1. Post-money SAFEs protect founders better than pre-money SAFEs

According to Carta data, nearly 80% of SAFEs issued in Q1 2025 were post-money SAFEs. This isn’t accidental. With a post-money SAFE, founders know exactly what ownership percentage they’re selling. With a pre-money SAFE, the actual dilution depends on how much total SAFE funding you raise—creating uncertainty and often greater-than-expected dilution.

If an investor proposes a pre-money SAFE in 2025, ask why. It’s increasingly non-standard.

2. The option pool matters more than most founders realize

The Carta data shows that Employee Stock Option Pools (ESOPs) typically range from 12% to 22% of fully diluted equity across different funding stages. Here’s what many founders miss: this pool is usually created just before an investment round and comes out of the founder/existing shareholder equity, not the new investor equity.

If you’re raising a Series A with a pre-money valuation of $40M and investors want a 15% option pool, that 15% is carved out of your ownership before the new investment arrives. This effectively reduces your valuation by the size of the pool.

Understanding this dynamic (covered well in Poland’s cap table guide and Feld’s Venture Deals) will save you from unexpected dilution.

3. Equal splits are increasingly common but not always optimal

The Carta data shows that 46% of two-founder teams now split equity equally (50/50), up from 32% in 2017. For three-founder teams, 27% split equally, up from 12% in 2015.

While equal splits can work well for teams with genuinely equal contributions, they can create problems if one founder contributes significantly more or if roles diverge substantially over time. Don’t default to equal splits just because they’re common—use frameworks from Slicing Pie and Foundational Equity to think through what’s actually fair for your specific situation.

Beyond the Books: Practical Tools

Reading these books is valuable, but knowledge becomes power when combined with practical tools:

Use Carta Launch (free until you raise $1M) to model your cap table scenarios. The platform lets you simulate what happens to ownership across multiple funding rounds with different terms. Before accepting any term sheet, model it in Carta to see the actual dilution impact.

Create a fundraising knowledge base: As you read these books, create a personal reference document with key terms, standard ranges, and your own red lines. This becomes your negotiating guide when you’re in the middle of fundraising pressure.

Join founder communities: Reading about fundraising is valuable, but learning from founders who’ve recently closed rounds is invaluable. Communities like South Park Commons, On Deck, or local founder groups provide context these books can’t.

Sign up for a Scale Up Masterclass: more than 4.000 participants have completed a Scale Up! program over the past seven years. From Canada to Cairo, Cape town to Oslo, founders, angels, mentors, faculty, executives and even VCs have built their skills with Scale Up! Join us for Scale Up Global!, Scale Up MENA! or Scale Up Africa Rising!

A Final Note on Information Asymmetry

VCs read these books. Angel investors read these books. Your lawyers (if you’ve hired good ones) know this material cold.

The information asymmetry in fundraising heavily favors investors. They’ve done dozens or hundreds of deals; you’re doing your first.

This reading list won’t eliminate that asymmetry, but it substantially reduces it. After absorbing these resources, you’ll recognize when terms are non-standard, when you’re being asked to accept unfavorable provisions, and—perhaps most importantly—when to push back and when to accept.

The difference between an informed founder and an uninformed one often shows up years later at exit. The founder who accepted a 2x participating liquidation preference without understanding it might discover that a $100M acquisition barely returns their money after investors take their share. The founder who negotiated that down to 1x non-participating might walk away with $15M instead of $2M.

That difference comes from understanding the content in these ten books.

Start With Foundational Equity

If you do nothing else, download and read Carta’s Foundational Equity report this week. It’s free, it’s current, and it contains data on:

- Solo founder vs. multi-founder dilution patterns

- Median valuation caps by round size

- Expected dilution benchmarks from pre-seed through Series D

- Advisor equity standards by stage

- Employee equity grant ranges by hire number

This single document will calibrate your expectations to market reality and help you spot when terms are outside normal ranges. Thanks, Peter Walker !

Then, based on where you are in your journey, pick the next 2-3 books from this list that match your immediate needs.

Have you read any of these books? What other entrepreneurial finance resources have you found invaluable? Let us know—we’re always looking to refine this list based on founder experiences.

This reading list was compiled based on 15+ years of working with founders across seed, venture, and growth stages in programs from Europe, Americas, MENA, Africa and APAC. The recommendations reflect resources that consistently help founders make better financial decisions and avoid costly mistakes