Continued from Part I (years T-2 -1). Read part I here, and Part III here.

Through the lens of Aisha Rahman, Founding Partner, Meridian Ventures With insights from: Rizal Tan, Co-Founder & General Partner And: Priya Nair, CEO, DataSync (Portfolio Company)

The investment period is where fund strategy meets market reality. For Meridian Ventures, Years 2-5 would test every assumption in our thesis—and force us to make decisions that would determine whether Fund I would succeed or fail. More importantly, it would teach us that building a world-class fundraising team was the key to our survival.

Year 2: Building the Portfolio

January-March: Deployment Accelerates

Year 2 began with unfinished business—we were still seeking to fill out our Fund I portfolio while simultaneously supporting our initial five investments.

The portfolio construction challenge:

Fund I targeted 12-15 investments. With $10M and roughly 30% reserved for follow-ons ($3M), we had $7M for initial investments. Average initial check: $450K-$600K.

Our investment period was 3-4 years, but best practice suggested deploying most capital in years 1-2 to allow adequate time for value creation before exits.

Target deployment pace: 4-5 investments per year in Years 1-2, slowing in Years 3-4.

Q1 investments:

Investment #6: HealthTech MY (February, Year 2) — Digital health platform connecting patients with specialists. Strong team from the Malaysian healthcare system. Complex regulatory environment, but a genuine market need. $450K investment.

Investment #7: PropTech.asia (March, Year 2) — Commercial real estate analytics. Data-driven approach to property valuation across South-East Asian markets. Two experienced founders from the real estate industry. $400K investment.

April-June: First Portfolio Challenges Emerge

By summer, reality started diverging from our investment memos.

DataSync: The early warning signs

Our first investment wasn’t developing as expected. The founding team—brilliant data scientists from Grab—struggled with go-to-market execution. Six months post-investment, they had built an impressive product with almost no customers.

Our board seat gave us visibility, but limited control. We pushed for them to hire a commercial co-founder. They resisted, believing the product would sell itself.

The VC’s dilemma:

This is where active ownership gets complicated. We had conviction in the market and product, but growing concerns about execution. Do we push harder and risk damaging the GP-founder relationship? Do we stay hands-off and hope they figure it out? Do we write more about our concerns in LP reports, potentially signaling problems prematurely?

We chose a middle path: supportive but direct feedback in board meetings, connected them with commercial advisors from our network, and documented our concerns internally while maintaining constructive external positioning.

Rizal’s perspective:

“DataSync taught us something important in Year 1: the gap between investment memo and portfolio reality. On paper, they were perfect—ex-Grab team, clear market need, technical excellence. In practice, they had a fundamental gap in commercial DNA. As investors, we could coach around the edges, but we couldn’t fix the team composition problem without their buy-in. That’s the limit of VC influence at the seed stage.”

July-December: Closing Out Year 2

More investments:

Investment #8: AgriTech ASEAN (August, Year 2) — Precision agriculture software for South-East Asian farms. Strong domain expertise from agricultural extension backgrounds. $350K investment.

Investment #9: EduScale ID (October, Year 2) — EdTech platform for corporate training, Indonesia-focused. First-time founder, but she’d been a customer of this category for years and understood the pain points intimately. $400K investment.

Investment #10: FinFlow (November, Year 2) — Subscription billing platform for regional SaaS companies. Two-time founder (previous exit to a strategic acquirer). More expensive than our typical deals—we paid a premium for founder pedigree. $550K investment.

Year 2 Summary:

Metric Value

Investments made 10 total (5 in Year 0, 5 in Year 1)

Capital deployed $4.1M (59% of initial allocation)

Portfolio value (estimated) $4.5M (modest markups)

Net IRR ~10%

TVPI 1.10x

DPI 0.0x (no distributions)

LP feedback (first annual meeting):

Our first annual LP meeting happened in November, Year 2. The feedback was mixed.

Positives: LPs liked our pace of deployment, the quality of our deal sourcing, and our transparent reporting.

Concerns: Multiple LPs questioned why we’d invested in 10 companies before having meaningful traction data from our earliest investments. Were we deploying too fast? Should we have waited to see DataSync progress before committing more capital? This was fair criticism. We defended our approach—the market window for seed deals doesn’t wait, and batch deployment is normal—but we heard the underlying anxiety.

Year 3: The J-Curve Bites Hard

January-March: Portfolio Divergence Accelerates

Year 3 revealed the brutal reality of seed-stage investing: outcomes diverge fast.

The winners emerging:

PayMalaysia signed a partnership with a major Malaysian bank, gaining access to 25,000 SME customers. Their MRR jumped from $15K to $45K in a single quarter.

CloudSEA landed their first enterprise customer and began generating real revenue. The founding team proved they could sell, not just build.

FinFlow—our expensive bet on the serial founder—launched and acquired 80 paying customers within three months. Unit economics looked strong.

The troubled middle:

LogiTech Asia was progressing but slowly. Their pilot customers liked the product but were reluctant to commit to scaled rollouts. The solo founder was burning out, handling everything herself.

SecureKL hit regulatory complexity we’d underestimated. Malaysian cybersecurity compliance required certifications that would take 12-18 months to obtain.

AgriTech ASEAN was pre-revenue and burning cash on R&D. The founders were making technical progress but had no commercial traction whatsoever.

The failures materializing:

DataSync continued its slow death march. By March, Year 3, they had signed only two customers—both small, low-ACV deals that didn’t validate the business model. Cash was running low.

The write-down conversation:

For the first time, we had to discuss portfolio write-downs with our LPs.

Our policy was to mark investments at fair value quarterly, based on either subsequent financing rounds or internal assessment. DataSync hadn’t raised follow-on capital, and our internal assessment suggested the company was worth significantly less than we’d paid.

The decision: Mark DataSync down by 50%. Our $400K investment was now carried at $200K.

This single write-down dropped our fund TVPI from 1.12x to 1.05x.

Grace Choo’s perspective (LP advisor, though not yet an investor):

“I remember Aisha calling to tell me about the DataSync write-down. She was clearly uncomfortable—admitting their first investment was struggling felt like a personal failure. But I actually gained confidence from that call. They weren’t hiding problems. They weren’t massaging valuations to look better. They were being straight about challenges. That’s exactly what I want to see from GPs.”

April-September: The Capital Crisis and Critical Decision

DataSync reaches the breaking point:

By July, DataSync had 4 months of runway remaining. The founding team came to us with two options:

Option A: Bridge financing to buy time for one more pivot attempt. They wanted $150K from existing investors to extend runway by 8-10 months.

Option B: Shut down the company, preserve remaining capital for investor return, accept failure.

This was our first major follow-on decision. The Fund Journey Map shows this moment clearly—the choice between doubling down and writing off.

The analysis:

We ran the numbers cold. DataSync had burned $500K (our $400K plus other investor capital) with almost nothing to show for it. The founding team had proven they couldn’t find early product-market fit despite multiple pivots. The market for SMB analytics was getting more competitive, not less.

A $150K bridge would increase our exposure to $550K in a company we’d already written down 50%.

Our decision: Don’t participate in the bridge. Let the company find other sources of capital or shut down.

This was painful. We liked the founders personally. We’d championed them to our LPs. Walking away felt like failure.

But the alternative was worse: good money after bad into a company that had demonstrated it couldn’t execute.

The aftermath:

DataSync couldn’t raise the bridge from other sources. In September, Year 3, they shut down and returned approximately $40K to investors. Our $400K investment became a $32K return—a 92% loss.

Priya Nair (CEO, DataSync) perspective:

“Looking back, Meridian made the right call. At the time, I was furious—I thought they were abandoning us. But we’d had 18 months to prove the model and hadn’t done it. Throwing more money at the problem wouldn’t have changed the fundamental issue: we were great at building product and terrible at selling it. I learned more from that failure than from anything else in my career. Two years later, I started a new company with a commercial co-founder from day one. That company is now doing $2M ARR. DataSync’s failure was my most important education.”

The Hard Lesson: We Need to Get Better at Fundraising

By late Year 3, with DataSync written off and the J-curve biting hard, we had a sobering realization.

“If we’re going to survive as a firm,” Rizal said one evening in our Bangsar office, “we need to raise Fund II. And we can’t go through the same scramble we did for Fund I. That nearly broke us.”

He was right. Fund I fundraising had been 18 months of desperation, cold outreach, and near-misses. We’d raised $10M through sheer determination, but we’d burned out in the process. And $10M wasn’t enough to build a sustainable management company.

We needed a systematic approach to fundraising. We needed a real fundraising team.

Building a World-Class Fundraising Team: The Game Changer

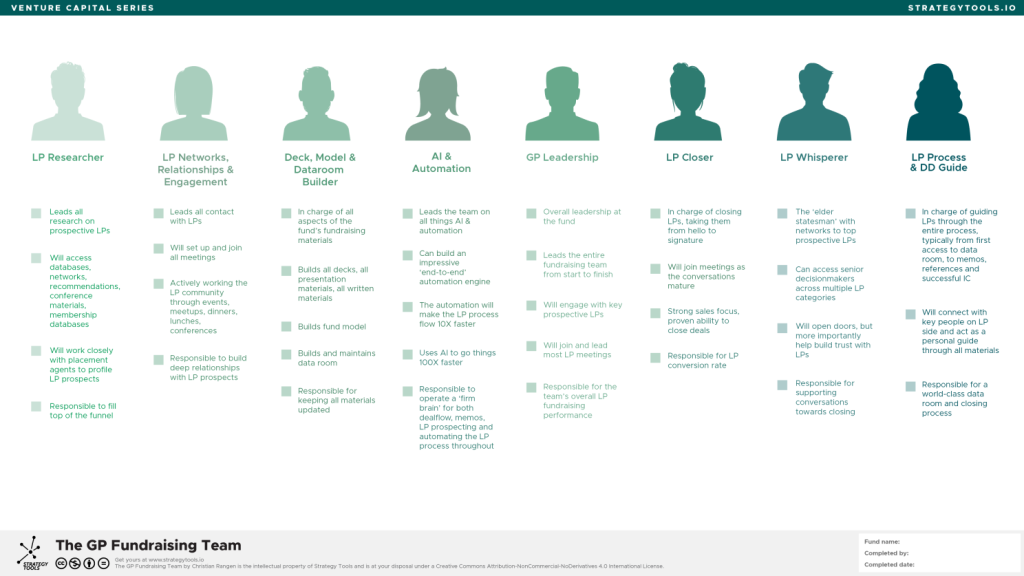

The canvas identifies eight distinct roles that drive successful LP fundraising. We didn’t have eight people—we never would for Fund II—but we deliberately covered each function:

Role Function Our Solution

LP Researcher

Leads all research on prospective LPs, fills top of funnel

Part-time analyst using ADB’s LP database and conference materials

LP Networks & Engagement

Builds deep relationships through events, conferences

Aisha – primary relationship builder through AVCJ, SuperReturn Asia

Deck, Model & Dataroom Builder

Builds and maintains all fundraising materials

Outsourced structure using Strategy Tools templates; Rizal maintained

AI & Automation

Builds automation engine to make LP process 10x faster

LP AI platform for persona practice + custom CRM workflows

GP Leadership

Overall leadership, joins and leads most LP meetings

Rizal – led all key meetings, responsible for overall LP performance

LP Closer

Takes LPs from hello to signature, strong sales focus

Split between Rizal and Aisha based on relationship warmth

LP Whisperer

Elder statesman with networks to top prospective LPs

Advisory board member from major family office + Jim, ex-ADB

LP Process & DD Guide

Guides LPs through entire process from data room to IC

Dedicated support from legal counsel + streamlined process docs

This systematic approach transformed our fundraising capability. Where Fund I had been desperate scrambling, Fund II would be organized execution.

Key changes we implemented:

1. Continuous LP engagement: We didn’t wait until we “started fundraising.” We maintained quarterly touchpoints with all Fund I LPs and prospective Fund II LPs from Year 3 onward.

2. Data room always ready: Instead of scrambling to build materials when an LP showed interest, we kept a perpetually updated data room.

3. LP persona customization: Different pitch materials for different LP types, practiced extensively using the Strategy Tools LP AI platform.

4. CRM discipline: Every LP interaction logged, follow-ups scheduled, relationship health tracked.

5. Advisory leverage: Our advisory board member opened doors we could never have opened ourselves.

The IFC Partnership: Becoming Institutional-Ready

One relationship proved transformative during our Fund II preparation: our connection to Grace Choo , Regional Lead at IFC (International Finance Corporation).

Grace had seen hundreds of emerging managers across Asia. She’d watched funds succeed and fail, scale and collapse. When we approached her in Year 3, we weren’t asking for investment (we knew our fund was too small for IFC at that stage). We were asking for guidance.

“We got immense support from Grace to understand how to evolve from Fund I to Fund II, and becoming institutional-scale ready,” I later told other emerging managers at an AVCJ panel.

Her guidance covered several critical areas:

On portfolio reporting: Institutional LPs expected quarterly reports with specific metrics. IFC had templates we could adapt.

On ESG integration: DFIs increasingly required ESG frameworks. Build these now rather than retrofit later.

On governance: Have an Advisory Committee and LP reporting structure that would scale.

On fund size: IFC typically couldn’t invest in funds under $50M, but if we performed well in Fund II, Fund III might qualify.

“Think of Fund II as your audition tape for institutional capital,” Grace advised. “Every decision you make, every report you write, every portfolio company you support—assume that institutional LPs will scrutinize all of it when you come back for Fund III.”

Andrew Senduk: Venture Partner for GTM Excellence

As our portfolio grew, we recognized a gap in our capabilities: go-to-market (GTM) execution. Many of our founders were technical experts who struggled with sales, marketing, and commercial scaling.

In Year 3, we brought on Andrew Senduk as a Venture Partner specifically to address this gap.

Andrew had spent 15 years building and scaling businesses across Indonesia, Malaysia, and Singapore. He’d led GTM for two successful startups (one acquired, one IPO’d) and understood the unique challenges of selling across South-East Asia’s fragmented markets.

Andrew’s perspective on joining Meridian:

“What attracted me to Meridian was their recognition that early-stage investing isn’t just about picking winners—it’s about helping those winners actually win. Most seed-stage founders in South-East Asia are technical builders who’ve never sold enterprise software or scaled a consumer product across multiple countries. That’s where I could add genuine value.”

Andrew worked with six of our Fund I portfolio companies on their GTM strategies:

• Sales process design for enterprise SaaS companies

• Market entry strategies for regional expansion

• Pricing and packaging optimization

• Customer success frameworks

His involvement became a key part of our LP pitch for Fund II: we weren’t just providing capital, we were providing hands-on GTM expertise that could meaningfully accelerate our portfolio companies’ growth.

Year 4: Portfolio Maturation and Fund II Launch

Portfolio Performance at Year 4:

Company Total Investment Status Current Value Multiple

DataSync $400K Shut down $32K 0.08x

PayMalaysia $450K Series A prep $2.2M 4.9x

CloudSEA $600K Growing $1.5M 2.5x

SecureKL $400K Bridge raised $350K 0.87x

LogiTech Asia $500K Turnaround $550K 1.1x

HealthTech MY $450K Growing $650K 1.4x

PropTech.asia $400K Growing $500K 1.25x

AgriTech ASEAN $350K Struggling $200K 0.57x

EduScale ID $400K Growing $600K 1.5x

FinFlow $550K Pre-Series A $1.8M 3.3x

Year 4 Fund I Metrics:

• Total invested: $4.5M (65% of initial allocation)

• Current portfolio value: $8.4M

• TVPI: 1.55x

• DPI: 0.01x

• Net IRR: ~18%

Fund II Strategy evolution

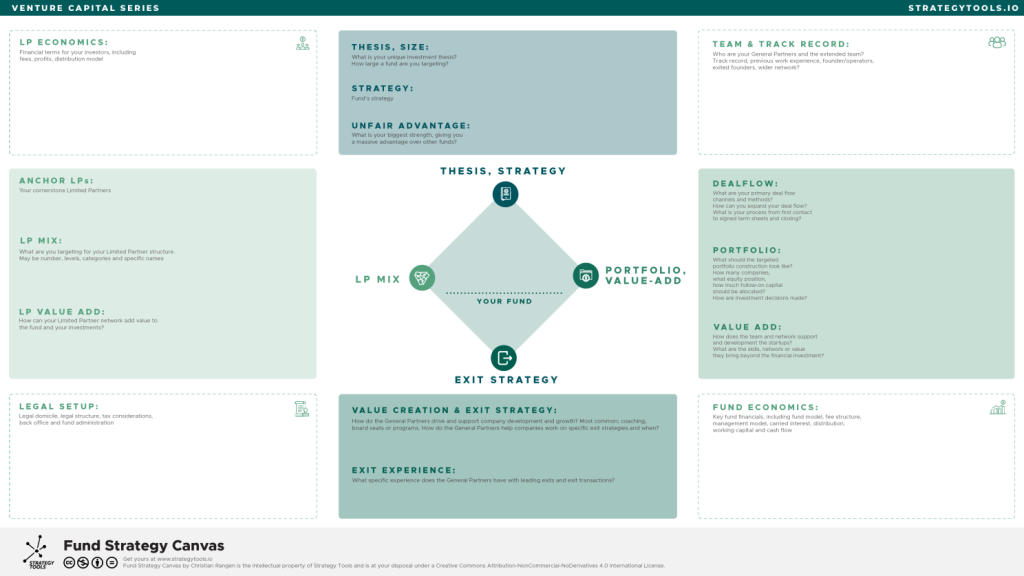

It was a webinar in March that led to team to step back and reflect. “Our fund II is not just a replica of fund I. We need to think far more strategically”. On the webinar, the team was introduced to the Fund Strategy Canvas, developed by Strategy Tools. Carving out a full-day offsite, the team sat down to complete the Fund Strategy Canvas together.

Fund Strategy Canvas: Meridian Ventures Fund II ($25M)

Fund Name: Meridian Ventures Fund II

General Partners: Aisha Rahman & Rizal Tan

THESIS, STRATEGY

Thesis & Size

Meridian Ventures Fund II is a $25M early-stage venture capital fund investing in B2B software and fintech companies across South-East Asia, with primary focus on Malaysia, Indonesia, Vietnam, and the Philippines.

Our thesis is built on three convictions:

First, South-East Asia’s digital economy is entering its enterprise phase. After a decade of consumer internet growth, the next wave of value creation will come from B2B infrastructure—payments, logistics software, enterprise SaaS, and vertical solutions that enable the region’s 70 million SMEs to digitize operations.

Second, the best founders in ASEAN are increasingly emerging from non-traditional backgrounds and geographies outside Singapore. Malaysia, Indonesia, and Vietnam are producing world-class technical talent with deep local market understanding. These founders are systematically overlooked by Singapore-centric VCs who rarely travel beyond Changi Airport.

Third, early-stage companies in emerging South-East Asian markets need more than capital. They need operational support—particularly in go-to-market execution, regional expansion strategy, and preparation for institutional follow-on rounds. GPs who combine capital with hands-on GTM expertise will generate superior returns.

Fund II targets $25M, representing a 2.5x step-up from our $10M Fund I. This size allows us to lead seed rounds of $500K-$1.5M while maintaining meaningful follow-on reserves for winners.

Strategy

Stage: Pre-seed to Seed, with selective Seed+ participation

Check size: $500K-$1.5M initial; up to $2M follow-on in winners

Geography: Malaysia (40%), Indonesia (35%), Vietnam/Philippines (25%)

Sectors: B2B software, fintech infrastructure, vertical SaaS, logistics tech

Target portfolio: 18-22 companies over 3-year deployment period

We invest at the earliest institutional stage—typically first or second money in after angels. Our sweet spot is technical founding teams with clear product vision but limited go-to-market experience. We help them build the commercial muscle to reach Series A.

Unfair Advantage

Our unfair advantage is the combination of three elements no other regional fund possesses:

Operator-investor team: Rizal spent 8 years building and scaling startups across Malaysia and Indonesia before becoming an investor. He’s lived the founder journey and speaks the language of operators, not just financiers.

Ground-level presence: We’re based in Kuala Lumpur, not Singapore. We travel to Jakarta, Ho Chi Minh City, and Manila monthly. We see deals 6-12 months before Singapore-based funds because we’re embedded in local founder communities.

GTM value-add through Andrew Senduk: Our Venture Partner has 15 years of enterprise sales and regional expansion experience. He works directly with portfolio companies on sales process, pricing strategy, and market entry—capabilities that differentiate us from capital-only investors.

TEAM & TRACK RECORD

General Partners

Aisha Rahman, Founding Partner

12 years in venture capital and corporate development. Former Principal at a mid-sized regional VC where she led 15+ investments across ASEAN. Board experience across fintech, SaaS, and logistics companies. MBA from INSEAD. Leads fund strategy, LP relations, and serves on 6 portfolio company boards.

Rizal Tan, Co-Founder & General Partner

8 years as operator, 4 years as investor. Former VP Business Development at a Series B payments company (acquired). Founded and sold a B2B marketplace in Malaysia. Leads deal sourcing, investment decisions, and portfolio company operational support. Deep networks across Malaysian and Indonesian founder communities.

Extended Team

Andrew Senduk, Venture Partner

15 years building and scaling businesses across Indonesia, Malaysia, and Singapore. Led GTM for two successful startups (one acquired, one IPO’d). Works with portfolio companies on sales process design, regional expansion, and commercial scaling. Not full-time but engaged across 6+ portfolio companies per fund.

Two Associates: Handle deal sourcing, due diligence support, and portfolio monitoring. One based in KL, one in Jakarta.

One Operations Manager: Fund administration, LP reporting, and back-office operations.

Track Record

Fund I Performance (as of Fund II launch):

Vintage: 2023

Size: $10M

Investments: 12 companies

TVPI: 1.55x

DPI: 0.02x (one small exit)

IRR: ~18%

Notable Fund I positions: PayMalaysia (4.9x paper, Series A prep), FinFlow (3.3x paper, growing rapidly), CloudSEA (2.5x paper, acquisition discussions). One complete write-off (DataSync), demonstrating follow-on discipline.

Prior Track Record (attributable deals from previous roles):

Aisha: 4 exits from prior fund, including 2 at 3x+ returns

Rizal: Personal angel portfolio of 8 investments, 2 exits at 5x+

LP MIX

Anchor LPs

Jelawang Capital ($4M commitment)

Regional thought leader in South-East Asian venture. Their rigorous due diligence and public commitment provides institutional validation. Jelawang serves on our Advisory Committee and actively supports our LP fundraising through introductions and co-hosted events.

Sarona Asset Management ($3M commitment)

Impact-focused fund-of-funds with emerging markets mandate. Their commitment signals ESG credibility and opens doors to other impact-oriented institutional LPs.

LP Mix Structure

LP Category Target Allocation Rationale

Fund-of-Funds (emerging manager programs) $7M (28%) Jelawang Capital, Sarona, Speedinvest, regional FoFs with SEA mandates

Regional Family Offices $6M (24%) Re-ups from Fund I plus new Singapore/Malaysian families

Fund I Re-ups (HNWIs, angels) $5M (20%) Strong re-up rate demonstrates LP satisfaction

Fund-of-fund $4M (16%) Dubai Future District Fund, SEA-MENA-oriented allocators

Strategic / Corporate $2M (8%) Corporate VCs seeking regional deal flow

GP Commitment$1M (4%), Increased from Fund I to demonstrate alignment

Target LP count: 18-22 LPs

Average commitment: $1.1-1.4M

Minimum commitment: $250K (to maintain fund I relationships)

LP Value Add

Our LP base isn’t just capital—it’s a strategic network:

Jelawang Capital: Portfolio company introductions, co-investment on larger rounds, thought leadership association

Sarona: ESG framework guidance, impact measurement support, introductions to impact-focused follow-on investors

Fund I HNWIs (exited founders): Direct mentorship to portfolio founders, customer introductions, hiring network access

Dubai Future District Fund: Middle East expansion pathway for portfolio companies, sovereign wealth fund network

Corporate LPs: Strategic partnership and M&A optionality for portfolio companies

LP ECONOMICS

Financial Terms

Term Fund II Structure

Management Fee

2.0% on committed capital during investment period

2.0% on invested capital thereafter

Carried Interest 20%

Preferred Return (Hurdle) 8%

GP Commitment 4% ($1M)

Waterfall European (whole-fund)

Fund Life10 years + two 1-year extensions

Investment Period 4 years

Distribution Policy

Distributions made as exits occur, subject to:

Return of LP capital contributions first

8% preferred return to LPs

80/20 split thereafter (LP/GP)

GP catch-up provision after hurdle achieved

Fee Offsets

100% of transaction fees, monitoring fees, and director fees received by GPs from portfolio companies are offset against management fees.

LEGAL SETUP

Fund Domicile: Labuan International Business and Financial Centre (IBFC), Malaysia

Fund Structure: Labuan Limited Partnership

Rationale for Labuan:

Tax-efficient structure for regional investments

Regulatory framework designed for investment funds

Lower setup and administration costs than Singapore VCC or Cayman

Acceptable to institutional LPs including DFIs

Geographic alignment with our KL base

Fund Administrator: Apex Fund Services (Singapore)

Legal Counsel:

Fund formation: Rajah & Tann (Singapore/Malaysia)

Portfolio investments: Local counsel in each jurisdiction

Auditor: Ernst & Young (Malaysia)

Tax Considerations:

Labuan entities benefit from 3% tax on net profits or flat RM20,000

No withholding tax on distributions to non-Malaysian LPs

Tax treaties in place with most LP jurisdictions

DEALFLOW

Primary Dealflow Channels

1. Founder Networks (40% of pipeline)

Rizal’s operator background generates direct founder referrals. Portfolio company founders introduce their peers. Our reputation for being “founder-friendly” creates inbound interest from founders who’ve heard about us through the ecosystem.

2. Ecosystem Partners (30% of pipeline)

Deep relationships with Cradle Fund (Malaysia), MDEC, 500 Startups (SEA), Antler, and regional accelerators. We’re the preferred follow-on investor for several accelerator programs because we move quickly and add operational value.

3. Angel/Syndicate Networks (20% of pipeline)

Co-invest relationships with AngelCentral Malaysia, Angel Investment Network Indonesia, and individual super-angels across the region. Angels bring us deals early; we bring them access to institutional rounds.

4. Proactive Sourcing (10% of pipeline)

Associates systematically track companies emerging from regional tech hubs, monitor funding announcements, and conduct outbound outreach to promising founders.

Dealflow Expansion Strategy

For Fund II, we’re expanding dealflow through:

Quarterly “Office Hours” in Jakarta, Ho Chi Minh City, and Manila

Content marketing (Aisha’s LinkedIn presence reaches 15,000+ regional followers)

Deeper accelerator relationships in Vietnam and Philippines (underserved in Fund I)

Investment Process

Stage Timeline Activities

Initial Screen 1 week

Partner review of deck/intro, quick pass/proceed decision First Meeting 1-2 weeks

60-minute founder meeting, both GPs attend, Deep Dive, Term sheet 1 1-3 weeks

Market analysis, reference calls, product review, Investment Committee 1 week

IC memo, partner discussion, decision, Term Sheet 2 & Close 1-4 weeks

Final terms negotiation, legal documentation, funding 1-4 weeks

Total process: 2-14 weeks from first meeting to close

Decision authority: Both GPs must approve; no solo deals

PORTFOLIO & VALUE ADD

Portfolio Construction Parameter

Target Number of investments 18-22 companies

Initial check size $500K-$1.5M

Follow-on reserves 35% of fund ($8.75M)

Target ownership 8-15% at entry

Concentration limit

No single investment >12% of fund

Follow-on Strategy

We reserve 35% of the fund for follow-on investments in winners. Follow-on decisions are made based on:

Company performance against milestones

Ability to maintain meaningful ownership

Quality of incoming investors

Risk/reward at new valuation

We explicitly do NOT do pro-rata follow-ons across the portfolio. Capital is concentrated in top performers. Fund I experience: followed on in 3 of 12 companies; those 3 represent 60% of portfolio value.

Investment Decision Framework

All investments must meet threshold criteria:

Team: Technical depth + commercial potential (or willingness to add commercial talent)

Market: $500M+ addressable market in ASEAN

Timing: Clear catalyst for why now

Fit: B2B/fintech focus aligned with thesis

Valuation: Entry price supporting 10x+ return potential

Value Add: How We Support Portfolio Companies

Board Engagement

GPs take board seats on all lead investments. Active participation in strategy, hiring, and fundraising decisions. Monthly check-ins with all portfolio CEOs.

GTM Support (Andrew Senduk)

Hands-on work with portfolio companies on:

Sales process design and optimization

Pricing and packaging strategy

Enterprise sales playbook development

Regional expansion planning

Customer success frameworks

Andrew engages with 6-8 companies per fund on structured GTM programs.

Talent Network

Curated network of 200+ executives and operators across ASEAN. Direct introductions for key hires. Quarterly portfolio talent events connecting companies with candidates.

Follow-on Fundraising

Warm introductions to Series A investors (Sequoia SEA, Vertex, East Ventures, Openspace, etc.). Preparation support for institutional fundraising. Data room and pitch coaching.

Peer Network

Quarterly portfolio CEO dinners. Slack community for real-time peer support. Annual offsite bringing together all portfolio founders.

EXIT STRATEGY

Value Creation & Exit Strategy

Value Creation Focus Areas:

During Years 1-3 (building phase):

Product-market fit validation

Initial revenue traction ($100K-$500K ARR)

Team building beyond founders

Market positioning establishment

During Years 3-5 (scaling phase):

Revenue acceleration ($500K-$3M ARR)

Unit economics optimization

Geographic expansion within ASEAN

Series A/B fundraising

During Years 5-8 (exit preparation):

Path to profitability or clear growth trajectory

Strategic relationship cultivation

Board composition optimization for exit

Financial and legal housekeeping

Exit Pathways:

Exit Type Expected % of Exits Typical Timeline

Strategic M&A (regional) 20% Years 4-7

Strategic M&A (global) 5% Years 5-8

Secondary sale 10% Years 4-6

IPO (rare at our stage) 5% Years 7-10

Write-off 60% Years 2-8

Exit Preparation Process:

Starting Year 2, we work with portfolio companies to:

Identify potential strategic acquirers

Build relationships with corporate development teams

Prepare management for M&A processes

Clean up cap table and legal structure

Develop exit-ready financial reporting

Exit Experience

GP Exit Track Record:

Aisha Rahman:

4 exits at prior fund, including 2 M&A transactions she led

Managed LP distributions and exit accounting

Board member through 3 acquisition processes

Rizal Tan:

Founded and sold B2B marketplace to strategic acquirer

Personal angel portfolio: 2 exits (1 acquisition, 1 secondary)

Operator perspective on founder exit psychology

Fund I Exits (to date):

SecureKL: Acquired for $2M (1.38x return)—managed full M&A process

DataSync: Orderly wind-down with capital return—demonstrated discipline

AgriTech ASEAN: Wind-down in progress

FUND ECONOMICS

Fund Model Summary

Item Amount

Fund Size $25,000,000

Management Fee (annual, investment period) $500,000

Management Fee (annual, post-investment period) $400,000 (on invested capital)

Total Management Fees (10-year life) $4,400,000

Available for Investment $20,600,000

Target Gross Multiple 3.0x

Target Net Multiple2.5x

Target Net IRR20%+

Management Company Economics

Annual management fee of $500K supports:

2 GP salaries (market-rate for regional VCs)

2 Associate salaries

1 Operations Manager salary

Office (KL headquarters + hot desks in SG, Jakarta)

Travel (significant—we’re on the ground across 4 countries)

Fund administration, legal, audit

LP relations and reporting

Cash Flow Reality:

Unlike Fund I (where we paid ourselves poverty wages), Fund II economics allow for sustainable GP compensation. This is critical for partnership stability and long-term firm building.

Carried Interest Distribution

Assuming 3.0x gross return ($75M exit proceeds) on $25M fund:

Distribution Amount

Return of LP Capital $25,000,000

8% Preferred Return to LPs $8,000,000

Remaining Proceeds $42,000,000

LP Share (80%)$33,600,000

GP Carried Interest (20%)$8,400,000

Total LP Returns: $66.6M on $25M invested (2.66x net)

GP Economics: $8.4M carried interest + ~$4.4M management fees over fund life

Working Capital

Fund II includes a modest working capital facility to bridge timing gaps between capital calls and expenses. This prevents the personal financial stress that characterized Fund I operations.

SUMMARY: WHY FUND II WILL SUCCEED

Meridian Ventures Fund II is positioned to deliver top-quartile returns because:

Proven Team: GPs with complementary skills, demonstrated partnership stability through Fund I challenges, and relevant operating experience.

Differentiated Strategy: Ground-level presence in underserved markets, combined with genuine GTM value-add through Andrew Senduk.

Strong Fund I Foundation: 1.55x TVPI with clear winners emerging, disciplined write-off decisions, and institutional-quality reporting already in place.

Right-Sized Fund: $25M is large enough to lead meaningful rounds but small enough to generate strong returns from regional exit valuations.

Institutional LP Base: Anchor commitments from Jelawang and Sarona provide validation and strategic value beyond capital.

Clear Path to Fund III: Fund II performance sets up institutional fundraise at $50M+, accessing DFI capital and achieving sustainable firm economics.

Fund II isn’t just an investment vehicle—it’s the foundation for building a permanent institution in South-East Asian venture capital.

Fund II Fundraising Begins

By mid-Year 3, we formally launched Fund II fundraising with a $25M target—2.5x our Fund I size.

The LP composition evolved significantly from Fund I:

LP Type Commitment

Jelawang Capital (anchor) $4M

Sarona Asset Management $3M

Dubai Future District Fund $2.5M

Speedinvest Emerging Manager Program $2M

Regional Fund-of-Funds (2) $5M

Fund I Re-ups (Family Offices, HNWIs) $6M

New HNWIs and Angels $2.5M

TOTAL $25M

Jelawang Capital: A Thought Leader Partnership

Among our Fund II LPs, Jelawang Capital stood out not just for their commitment size but for their role in the ecosystem.

Jelawang had established themselves as thought leaders in South-East Asian venture, publishing research on emerging manager performance, hosting convenings for GPs and LPs, and advocating for ecosystem development across the region.

Their due diligence process was rigorous—more intensive than any other LP we’d encountered. But that rigor came with genuine partnership. Once they committed, they became active supporters of our firm, making introductions to other LPs, providing feedback on our portfolio strategy, and including us in their thought leadership events.

“Having Jelawang as an anchor LP gave us credibility that we couldn’t have purchased at any price,” Rizal later reflected. “When other LPs saw that Jelawang had done deep due diligence and committed, it reduced their perceived risk in backing us.”

Fund II closed in 14 months—4 months faster than Fund I. The difference was our systematic fundraising approach. We had LP coverage across every major category. We had materials ready. We had a process. We weren’t scrambling; we were executing.

Year 5: Fund II Deployment and Fund I Value Creation

Fund II First Investments:

With $25M to deploy, Fund II allowed us to write larger checks ($500K-$1.5M) and target slightly later-stage opportunities (seed+ to Series A).

Fund II investments (Year 5):

• Investment #1-3: Three seed rounds averaging $800K

• Investment #4-5: Two Series A participations averaging $1.2M

• Total deployed Year 5: $5.2M (21% of fund)

Fund I Portfolio Events:

PayMalaysia closes Series A (October, Year 5): $5M round led by Jungle Ventures, a top-tier regional VC. Our follow-on: $200K to partially maintain position. PayMalaysia was now valued at $18M; our position worth approximately $3.5M on $650K invested (5.4x).

SecureKL acquired (November, Year 5): In a surprise development, SecureKL was acquired by a regional cybersecurity company for $2M. Our $400K investment returned $550K—a modest positive outcome (1.38x) after years of struggle. First actual exit and DPI generation!

AgriTech ASEAN shuts down (December, Year 5): After 3+ years with no commercial traction, AgriTech’s board and founders decided to wind down the company. Our $350K investment returned approximately $50K from remaining cash. Second complete write-off.

Year 5 Fund I Metrics:

• Total invested: $5.2M (75% of initial allocation)

• Current portfolio value: $11.5M

• Distributions (DPI): $600K (SecureKL exit + DataSync wind-down + AgriTech wind-down)

• TVPI: 2.15x

• DPI: 0.12x

• Net IRR: ~26%

Key Takeaways from Part II

For fund managers in their investment period:

1. The J-curve is real and painful. Years 2-5 will feel like failure even when you’re building a successful portfolio. Communicate this to your LPs early and often.

2. Portfolio mortality is normal. Expect 30-80% of seed investments to fail completely. The key is limiting exposure to losers while maximizing exposure to winners.

3. Follow-on decisions define returns. Our Fund I returns were driven by concentrated follow-on in PayMalaysia and FinFlow. Spray-and-pray follow-on destroys returns.

4. First exit matters more than its size. SecureKL’s 1.38x return was modest, but generating actual DPI established our credibility for Fund II.

5. Build your fundraising team before Fund II. Use the GP Fundraising Team canvas to systematically cover all eight roles, even with a small team.

6. Fund II timing is strategic. Starting Fund II in Year 3-5, before Fund I exits, is standard practice. LPs understand the cycle.

Grace Choo’s final perspective on Part II:

“By Year 5, I’d moved from cautious optimism to genuine confidence in Meridian. They’d made hard decisions, communicated transparently, and generated reasonable paper returns. More importantly, they’d maintained partnership stability through challenging years. Fund II felt like a natural evolution, not a leap of faith. I told them we’d be interested in exploring a Fund III commitment if they could reach $50M.”

Read part III: Value Creation, Fund III, and Institutional Arrival (Years 6-7).

If you have not already read it, check out part I, the early years.