Continued from Part I (years T-2 -1). Read part I here, and Part II here.

Through the lens of Aisha Rahman, Founding Partner, Meridian Ventures With insights from: Rizal Tan, Co-Founder & General Partner And: Ahmad Ismail, CFO, PayMalaysia (Portfolio Company)

By Year 5, we had deployed most of Fund II and were generating the track record that would define our institutional future. The question was no longer whether we could survive—it was whether we could scale.

Year 6: Fund I Harvest Mode and Fund III Preparation

Fund I Portfolio Status:

Company Total Investment Status Current Value Multiple

DataSync $400K Exited (failure) $32K 0.08x

PayMalaysia $650K Series B prep $6M 9.2x

CloudSEA $700K Acquisition talks $2.5M 3.6x

SecureKL $400K EXITED $550K 1.38x

LogiTech Asia $600K Growing $1.2M 2.0x

HealthTech MY $550K Growing $1.4M 2.5x

PropTech.asia $500K Profitable $900K 1.8x

AgriTech ASEAN $350K Exited (failure) $50K 0.14x

EduScale ID $500K Series A complete $1.8M 3.6x

FinFlow $650K Series A complete $3.2M 4.9x

Year 6 Fund I Metrics:

• Portfolio value: $17.5M (8 remaining companies)

• Total distributions: $632K

• TVPI: 2.8x

• DPI: 0.13x

• Net IRR: ~32%

CloudSEA Acquisition:

In June, Year 6, CloudSEA was acquired by a regional enterprise software company for $8M. Our proceeds: $2.2M on $700K invested (3.1x).

This was our second meaningful exit and dramatically improved our DPI story.

Fund I Post-CloudSEA:

• Total distributions: $2.85M

• DPI: 0.57x

• TVPI: 3.0x

Fund III: The Institutional Leap to $50 Million

Fund III represented our transition from emerging to established manager. At $50M, we could finally access the institutional capital that had been out of reach for our first two funds. But doing so, required next level fundraising strategy.

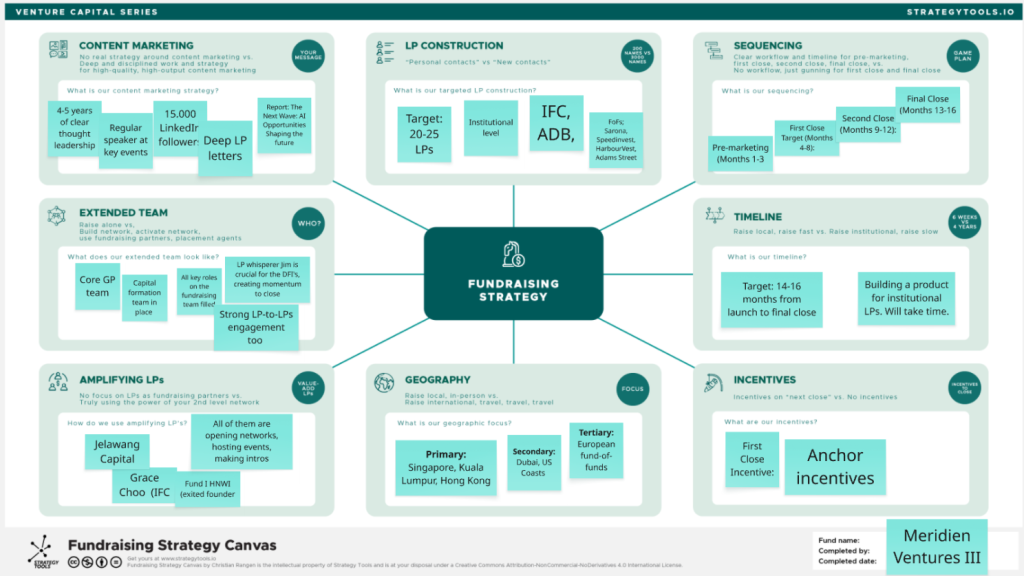

Fundraising Strategy Canvas: Meridian Ventures Fund III ($50M)

Fund Name: Meridian Ventures Fund III Completed by: Aisha Rahman & Rizal Tan Completed date: May 5th

Content Marketing (Your key message)

Our Fund III content strategy builds on five years of thought leadership. Aisha publishes monthly insights on South-East Asian venture trends via LinkedIn and our firm blog, reaching 15,000+ followers across the region. We co-author research with FoF’s on emerging manager performance in ASEAN markets. Rizal speaks regularly at AVCJ, SuperReturn Asia, and regional LP convenings. Our quarterly LP letters have become known for transparent, detailed portfolio analysis—several prospective LPs cited these as reasons for taking initial meetings. For Fund III, we’re producing a signature report on “The Next Wave: AI Opportunities Shaping the future” to position our revised thesis.

LP Construction (200 Names vs 3000 Names)

Fund III targets 20-25 LPs with an average commitment of $2-2.5M. Our construction starts with warm relationships: 12 re-up conversations with Fund I/II LPs (targeting 80% re-up rate), plus 8 qualified new institutional prospects. We’re not casting wide—we’re going deep on LPs where we have genuine fit.

Our primary list includes: IFC and ADB (DFI mandate alignment), 4 fund-of-funds with emerging manager programs (Sarona, Speedinvest, HarbourVest, Adams Street), 3 regional pension funds beginning SEA allocations, 2 American foundations with Asia impact mandates, and 3 corporate VCs seeking regional deal flow access. Secondary list adds 15 family offices across Singapore, Hong Kong, and the Gulf.

Sequencing (Game Plan)

Pre-marketing (Months 1-3): Soft conversations with Fund I/II LPs to gauge re-up appetite and gather reference feedback. Update all materials, refresh data room, finalize Fund III terms.

First Close Target (Months 4-8): Secure anchor commitments from Jelawang Capital ($6M target) and one DFI (IFC at $8M). These two anchors unlock the rest of the raise.

Second Close (Months 9-12): Convert fund-of-funds and re-ups. Target $35M cumulative.

Final Close (Months 13-16): Complete pension fund and foundation conversations. Close at $50M.

Extended Team (Who?)

We’re not raising alone. Our extended team includes: Jim, the ex-ADB (warm introductions to DFI network), our advisory board member from a major Malaysian family office (opens doors across Gulf family offices), Jelawang Capital’s LP relations team (co-hosting events where we’re featured), our Fund II co-anchor LP who now sits on two foundation boards (direct introductions), and a placement agent for European institutional LPs only (Eaton Partners, success-fee basis).

As always, Andrew Senduk and his army of AI agents supports by presenting our GTM value-add story to LPs evaluating our portfolio support capabilities. We also brought in people like Jen Braswell and Paola Ravacchioli to guide us into the world of institutional readiness.

The biggest difference, now we have a full capital formation team, full-time. That’s a game-changer.

Timeline (6 Weeks vs 4 Years)

Target: 14-16 months from launch to final close. We’re raising institutional, so we accept longer cycles. DFIs like IFC require 6-9 months from first meeting to IC approval. Pension funds need 4-6 months minimum. We’ve built relationships with target LPs over the past 2 years specifically to compress these timelines. Fund II closed in 14 months; we’re targeting similar pace for Fund III despite larger size because our LP relationships are now mature and our track record is proven.

Amplifying LPs (Value-Add LPs)

Three LPs serve as active amplifiers for Fund III:

Jelawang Capital: As anchor, they’re actively referring us to their LP network and co-hosting a webinar on SEA emerging managers where Meridian is featured.

Grace Choo (IFC): Beyond their commitment, IFC’s involvement signals institutional validation. We’ll reference their due diligence process and commitment in all LP conversations.

Fund I HNWI (exited founder): Now a respected angel investor, he’s made personal introductions to three family offices in his network who are exploring VC allocations.

Geography (Focus)

Primary: Singapore, Kuala Lumpur, Hong Kong (in-person intensive). These three cities cover 70% of our target LP base.

Secondary: Dubai (6 trips planned for Gulf family offices and sovereign-adjacent capital), Washington DC (IFC HQ, 4 trips), San Francisco (2 American foundations, 5 trips).

Tertiary: European fund-of-funds handled primarily via placement agent with 3 Rizal trips to London/Amsterdam.

We’re not trying to cover the world. Geographic focus means deeper relationships in fewer places.

Incentives (Incentives to Close)

First Close Incentive: LPs committing by first close receive most-favored-nation status on any future side letter terms and priority co-investment allocation on the first three Fund III deals.

Anchor Incentive: Jelawang Capital’s $6M anchor commitment came with a seat on our Advisory Committee and quarterly strategic calls with GPs beyond standard LP updates.

No fee discounts. We learned from Fund I that fee discounts create LP management complexity and signal desperation. Our 2/20 terms are firm. Value-add comes through access and relationships, not economics.

Summary: Why Fund III Will Close

Fund III succeeds because we’ve built the infrastructure over four years:

1. Track Record: Fund I at 2.8x TVPI with 0.6x DPI; Fund II performing at 1.6x TVPI in Year 2

2. LP Relationships: 80%+ expected re-up rate from existing LPs

3. Institutional Readiness: IFC-grade reporting, ESG frameworks, governance already in place

4. Anchor Momentum: Jelawang and IFC commitments create herd effect for remaining LPs

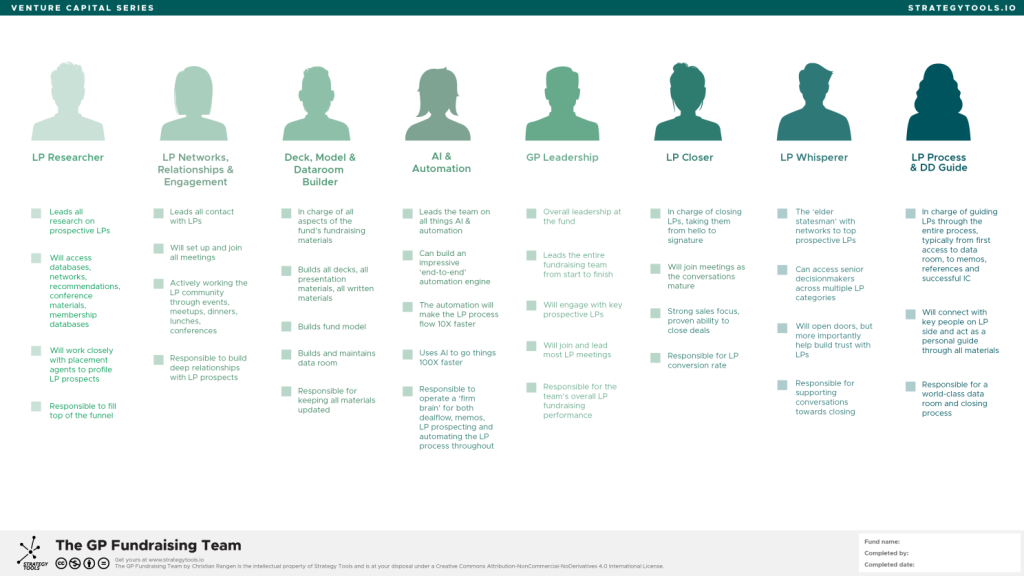

5. Team Coverage: All 8 GP Fundraising Team roles systematically covered

6. Geographic Discipline: Focused presence in 3 primary cities, not scattered globally

We’re not hoping to raise $50M. We have a plan to raise $50M.

The Fund III LP roster showed our journey from emerging to institutional:

LP Type Commitment

IFC (International Finance Corporation) $8M

Jelawang Capital (top-up) $6M

Fund-of-Funds (top-ups x3) $10M

Employees Provident Fund (EPF / KWSP) $5M

Regional pension fund (1) $1M

American Foundations (2) $5M

Corporate VCs / Strategics (3) $8M

Fund I/II Re-ups $7M

TOTAL $50M

IFC: The Institutional Validation

When IFC committed $8M to Fund III, it represented the culmination of a eight-year relationship.

Grace’s guidance during Fund I and II had prepared us for IFC’s due diligence process—one of the most rigorous in the industry. When the IFC team reviewed our fund, they found:

• ESG frameworks already in place

• LP reporting that met institutional standards

• A governance structure that could scale

• A track record of transparent, disciplined decision-making

• A clear investment thesis with demonstrated execution

“Meridian had done the hard work of institutionalization before they needed to,” an IFC investment officer noted during our closing celebration. “That’s rare for emerging managers. Most try to retrofit institutional practices after they want institutional capital. Meridian built the foundation first.”

Analyzing the LP outcome scenarios for EPF / KWSP

One particularly valuable preparation was the extended masterclass we did on the LP outcome scenarios. This actually happened in Lausanne, Switzerland, where we participated in IMD’s Venture Asset Management program. Here we met Jim and Heidi, from ZKB. We got to develop and then truly practice using the LP outcome canvas. Enrique pushed us hard on this. This was truly transformative.

We did not know it at the time, but just months later we would find ourselves in exactly the same position, when the investment team at EPF/KWSP started discussing their LP outcome analysis with us. Suddenly, we realized we could hold our ground and discuss, even negotiate with them on LP outcome models. Looking back, that was probably the moment it clicked, ‘now we are truly institutionally ready’.

Read the full LP outcome analysis from EPF/KWSP here.

The 20-Month Fundraising Cadence

Fund III closed in early Year 7, meaning we had raised three funds in seven years—a new fund approximately every 20 months.

This aggressive pace was only possible because of the fundraising infrastructure we’d built:

• LP relationships maintained continuously (not just during fundraising windows)

• Data room always updated and ready

• Fundraising team roles clearly defined across our small team

• AI and automation tools accelerating LP research and outreach

• Process-driven approach to LP conversion

Year 7: The Firm Today

By the end of Year 7, Meridian Ventures managed $85M across three funds:

Fund Size Vintage Status

Fund I $10M Year 0 Harvesting

Fund II $25M Year 2 Value Creation

Fund III $50M Year 4 Deploying

Our team had grown from 2 founders to 8 people: 2 GPs, 1 Venture Partner (Andrew Senduk), 2 Principals, 2 Associates, and 1 Operations Manager, as well as a full team of AI agents.

We’d invested in 32 companies across South-East Asia. Four exits completed. One potential unicorn in the making (PayMalaysia, now valued at $60M+ and heading toward Series C).

We were no longer emerging managers. We were an established firm with institutional credibility, consistent returns, and a platform that would outlast any individual partner. Of course, with three funds, we now need to start generating exits and DPI back to our LPs. That’s the next step of the journey.

Key Recommendations for Emerging Fund Managers in South-East Asia

Having navigated the journey from concept to $85M under management, here are the recommendations we would give to emerging managers starting today in South-East Asia:

1. Start Smaller Than You Think

Our original target of $30M for Fund I would have been impossible to raise. $10M was achievable—barely. In emerging markets, fund size credibility must be earned gradually. A successfully deployed $10M fund opens doors that no amount of pitch materials can open for a $50M first fund.

2. Understand the Economics Brutally

A 2% management fee on a $10M fund is $200,000 per year. After fund administration, legal, office, and travel, you’ll be paying yourselves poverty wages. Plan for this. Either have personal runway, alternative income sources, or extremely understanding life partners. The economics only work at scale—which means Fund II and III are not optional; they’re survival requirements.

3. Invest in Fundraising Infrastructure Early

Use the GP Fundraising Team canvas to build systematic fundraising capability, even if you’re just two people. Define who covers each role. Use AI and automation tools aggressively. Define your LP personas. Nail your LP Value proposition. Maintain your LP CRM continuously. The difference between our Fund I scramble and Fund II execution was entirely about infrastructure.

4. Leverage Ecosystem Builders

Organizations like IFC, ADB, Cradle Fund, and Jelawang Capital exist to support ecosystem development. They want emerging managers to succeed. Engage with them early—not for capital, but for guidance, connections, and credibility. Our relationships with Grace Choo at IFC and Craig and Ian at ADB were transformative years before they led to any investment.

5. Build Value Creation Capabilities

South-East Asian founders often need more support than capital. Andrew Senduk’s GTM expertise became a genuine differentiator for our fund. Think about what operational value you can genuinely provide, and build that capability deliberately. LPs increasingly want to see portfolio support, not just deal access.

6. Accept the LP Evolution Timeline

Fund I will likely be friends, family, HNWIs, and angels. Fund II will add some early institutional elements—fund-of-funds, emerging manager programs. Fund III is when major institutional capital becomes accessible. Don’t fight this progression; plan for it. Each fund stage prepares you for the next.

7. Maintain a Fundraising Cadence

Raising a new fund every 20-24 months sounds aggressive, but it’s actually survival strategy. It keeps LP relationships warm, demonstrates traction, and builds the AUM necessary for sustainable GP economics. Start thinking about Fund II long before Fund I even closes.

8. Be Transparent About Challenges

Our first write-off was painful to communicate to LPs. But our transparent handling of that failure—and our discipline in not throwing good money after bad—built credibility that paid dividends in Fund II and III. LPs expect some failures. What they’re watching for is how you handle them.

9. Invest in Education Continuously

The Fund Manager! Masterclass transformed our approach. Strategy Tools’ LP AI platform sharpened our pitching. Industry conferences, peer networks, and continuous learning aren’t luxuries—they’re requirements for staying competitive in a rapidly evolving industry.

10. Remember It’s a 15-Year Journey

The Fund Journey Map shows a 15-year cycle from idea to final distribution. We’re only at Year 7. The hardest part—converting paper gains to actual DPI—is still ahead. This is a career commitment, not a quick path to wealth. Make sure you’re in it for the right reasons and with the right partners.

Final Reflections

Rizal’s reflection:

“Six years ago, Aisha and I were two people in a converted shophouse, maxing out credit cards and wondering if anyone would ever trust us with institutional capital. Today, we manage $85M across three funds with IFC as an LP and genuine institutional credibility. Fund I’s emerging returns aren’t the highest in the industry, but they’re solid, repeatable, and built the foundation for everything that followed. The Fund Journey Map captures the phases, but what it can’t capture is the emotional journey—the anxiety of Year 0, the relief of first close, the devastation of our first write-off, the joy of our first major exit. This business is deeply human. That’s what makes it worth doing.”

Aisha’s reflection:

“If I could give one piece of advice to emerging managers starting today in South-East Asia, it would be this: the fund journey is a marathon, not a sprint. Every phase has its challenges and rewards. Year T-2 felt impossible; Year 4 felt like vindication; Year 6 feels like we’ve just begun. Through all of it, the constants were partnership stability, LP transparency, and founder-first investing. Those principles guided every decision. They’ll guide Fund IV and beyond.”

The fund journey continues.

Read Part I (years T-2 -1), I here, and Part II here.

About the Fund Journey Map and GP Fundraising Team Canvas

The Fund Journey Map by Strategy Tools visualizes the complete 15-year lifecycle of a venture capital fund, from early idea through final distribution. It captures the key decision points, risks, and milestones that define the GP experience. Based on work with 100’s of emerging fund managers, the Fund Journey Map is designed to help emerging managers successfully navigate the full fund journey.

The GP Fundraising Team canvas identifies the eight roles that drive successful LP fundraising, from LP Researcher through LP Process & DD Guide. Both tools are part of Strategy Tools’ Venture Capital Series.

Download the Fund Journey Map, GP Fundraising Team canvas, and explore our full suite of GP accelerators and venture capital programs at strategytools.io

Ready to start your fund journey?

Join the Fund Manager! Masterclass to learn from experienced GPs, practice with our Fund Manager simulation, and build the skills needed to launch and manage successful venture capital funds. Learn more.

This article is part of the Venture Capital Series at Strategy Tools, helping fund managers, LPs, FoFs and ecosystem builders develop better venture capital ecosystems around the world.

About the Author:

Christian Rangen is a strategy advisor and business school faculty. He works with ambitious ecosystem developers, innovation agencies, venture funds, national fund-of-funds and governments on building better VC firms and VC ecosystems. He runs GP Accelerators and GP Masterclasses globally.

A huge thanks to Scott Newton Rick Rasmussen Efe (Braimah) Barber Winnie Odhiambo Jen Braswell Paola Ravacchioli Jim Pulcrano Enrique Alvarado Hablützel Marijn Wiersma Jessica Low Jessica Espinoza Marième Diop Sanjana Raheja Rumbi Makanga for inspiring this 3-part story