From Fund I ($10M) to Fund III ($50M) in Six Years. A Three-Part Series on Building a South-East Asian Venture Capital Firm from Scratch

Written by Christian Rangen, advisor to VC funds, Fund-of-funds, faculty,

Written through the lens of Aisha Rahman, Founding Partner, Meridian Ventures With insights from: Rizal Tan, Co-Founder & General Partner, Meridian Ventures-

The people and companies are largely fictional for the purpose of this article, based on the Fund Journey Map and GP Fundraising Team canvas by Chris Rangen, Strategy Tools.

Part I: From Idea to First Close (T-2 to Year 1)

The journey from “we should start a fund” to actually managing institutional capital is longer, harder, and more humbling than almost any first-time fund manager expects. Here’s how one South-East Asian emerging manager navigated those critical early years—and learned the hard way that fundraising requires a completely different skill set than investing.

It’s 11:47 PM in Kuala Lumpur, and I’m staring at a spreadsheet that makes no sense. We’ve been working on our fund concept for eighteen months now, and I still can’t articulate why a family office would trust us with $2 million when we’ve never managed a fund before.

Rizal is asleep on the couch in our tiny shared office—a converted shophouse in Bangsar that we’re renting month-to-month because we can’t commit to a lease until we know if this fund will actually happen.

That was Year T-1. Six years later, we would be managing $85 million across three funds—Fund I ($10M), Fund II ($25M), and Fund III ($50M)—having raised a new fund every 20 months on average. We would establish ourselves as one of South-East Asia’s most consistent emerging-stage performers and a genuine thought leader in the region’s venture ecosystem.

But in that moment? I genuinely didn’t know if we’d make it past first close.

This is the story of our fund journey—the real one, not the polished version we tell at conferences. If you’re an emerging manager in South-East Asia, or thinking about becoming one, pay attention to the ecosystem builders who helped us along the way. And pay close attention to our fundraising evolution—because that’s what ultimately made the difference between survival and success.

Year T-2: The Idea Takes Shape

The Spark

Rizal and I met at a fintech conference in Singapore in 2017. He was running business development for a Series B payments company backed by Golden Gate Ventures; I was a principal at a mid-sized regional VC that was, frankly, underperforming.

Over teh tarik at a mamak in Petaling Jaya, we complained about the same things: VCs who didn’t understand founders. Decision-making processes that took months. Partners who’d never built anything themselves. The disconnect between what South-East Asian founders needed and what most regional funds delivered.

“We should start our own fund,” Rizal said, half-joking.

“We should,” I replied, not joking at all.

That conversation planted a seed that would consume the next three years of our lives.

The Reality Check

Starting a fund isn’t like starting a company. You can’t bootstrap it. You can’t build an MVP and iterate. You need LP commitment before you can do anything—and LP commitment doesn’t flow to people without track records.

We spent the first six months of Year T-2 doing what I now call “the reality audit.”

Market Opportunity Assessment: We mapped the South-East Asian early-stage landscape, with particular focus on Malaysia, Indonesia, Vietnam, and the Philippines. What we found was both encouraging and terrifying. Encouraging: a genuine gap existed for founder-friendly, operationally-focused pre-seed and seed investors in the $200K-$1M range. Singapore had become expensive for startups, and regional founders needed alternatives that understood local markets. Terrifying: at least 30 other groups were circling the same opportunity, and several established Singapore VCs were beginning to look downstream.

The Malaysian Ecosystem Landscape: Early in our research, we discovered the critical role of Cradle Fund in Malaysia’s startup ecosystem. Cradle had been nurturing early-stage companies since 2003, providing grants and coaching that created the very dealflow we hoped to invest in. Understanding Cradle’s portfolio became essential to our thesis—many of our future portfolio companies would be Cradle alumni. We also mapped the roles of MDEC, MaGIC, and various state-level initiatives. South-East Asia’s venture ecosystem wasn’t just Singapore anymore.

Team Capabilities Audit: Between us, we had twelve years of relevant experience. Rizal had operator credibility from his startup years and deep fintech knowledge. I had investment experience, but as a principal, not a decision-maker. Neither of us had carried interest (the profit share that defines GP economics). Neither of us had ever raised institutional capital.

Investment Thesis Development: This is where most emerging managers fail first. They have a vague idea—“we invest in great founders”—but no differentiated thesis that answers the question every LP will ask: Why you? Why now? Why this strategy?

We spent three months developing our initial thesis. Early-stage generalist tech across South-East Asia, with initial focus on Malaysia and Indonesia, concentrating on B2B software and fintech, with a contrarian bet on founders from non-traditional backgrounds who were overlooked by establishment VCs. Check sizes of $200K-$800K, targeting 12-15 investments over a three-year deployment period.

The Honest Assessment: By the end of Year T-2, we had a thesis we believed in, complementary skills, and genuine founder networks from our previous roles. What we didn’t have: LP relationships, a track record as GPs, or any idea how to actually raise a fund.

The Fund Manager! Masterclass: A Turning Point

In late Year T-2, we made a decision that would fundamentally change our trajectory: we enrolled in the Fund Manager! Masterclass run by Strategy Tools.

“It blew our minds,” Rizal later told other emerging managers. “We thought we understood venture capital because we’d worked in the industry. The Masterclass showed us we didn’t understand the first thing about running a VC firm; and definitely not about delivering net DPI back to LPs.”

The Masterclass covered fund economics, LP prospecting, portfolio construction, value creation and DPI in ways that academic programs never touched. But the real value was the simulation component—practicing LP pitches, running investment committee discussions, and navigating the inevitable cash flow crunches that plague emerging managers. It was intense, but incredible.

We left the Masterclass with a completely revised approach:

• Our fund target dropped from $30M (too ambitious for first-time managers in South-East Asia) to $10M (achievable and sustainable).

• Our thesis sharpened around specific value-add we could provide: operational support for B2B go-to-market.

• We understood the brutal economics of small funds—and planned accordingly.

Most importantly, we had a realistic understanding of the economic challenges ahead. The Masterclass didn’t make fundraising easy. It made us prepared for how hard it would actually be.

Key Learnings from Year T-2

Looking back, we made two critical decisions that year that shaped everything that followed.

Decision 1: We chose generalist over specialist. Many advisors told us to pick a vertical—“focus on fintech only” or “own the Malaysian SaaS space.” We resisted. Our thesis was that the best opportunities at seed stage in emerging South-East Asian markets often came from unexpected intersections. A generalist approach gave us flexibility but made our LP pitch harder. We’d need to defend that choice hundreds of times.

Decision 2: We committed to doing this together or not at all. Rizal had a standing offer to return to his old company as VP of Strategy. I had recruiters calling about partner-track roles at larger regional funds. We agreed: if we hadn’t reached first close within two years, we’d both move on. That deadline created urgency but also alignment.

Year T-1: The Fundraising Education Begins

(And it was a very hard school)

January-March: Building the Foundation

Year T-2 started with a sobering realization: we knew nothing about LP fundraising.

I’d spent years helping portfolio companies raise capital from VCs. The dynamic there is relatively straightforward—founders pitch investors who make decisions in weeks. LP fundraising is an entirely different animal.

The first quarter was pure education:

We read every book on fund formation we could find. We attended two LP conferences as observers (paying full tickets we couldn’t afford). We cold-called fifteen fund managers who’d raised first-time funds in South-East Asia, asking them to share their experiences. Most were incredibly helpful.

What we learned was humbling:

The average first-time fund takes 18-24 months to raise. Many take longer. Most never close at all. In fact, 75% of all GP teams give up before their coveted first close. LPs receive hundreds of fund pitches per year and invest in perhaps 2-3% of them. First-time managers face a structural disadvantage: LPs prefer to re-up with existing managers rather than take risk on unproven GPs.

Grace Choo’s perspective (Regional Lead, IFC):

“When I look at emerging managers, I’m not just evaluating the strategy. I’m evaluating the people and their ability to survive the inevitable hard times. Most first-time funds face an existential crisis within the first three years—deal-flow problems, portfolio blowups, partnership tensions. The question is: do these GPs have the resilience and alignment to get through it together?”

April-June: Legal Setup and GP Economics

We incorporated our management company in April. This sounds simple. It wasn’t.

The legal complexity almost derailed us:

Fund structure: Labuan IBFC? Singapore VCC? Cayman Islands? Each jurisdiction had different tax implications, different regulatory requirements, different costs. We spent $25,000 on legal fees just to understand our options—money we funded personally from savings.

GP commitment: LPs expect GPs to have meaningful skin in the game, typically 1-3% of fund size. For a $10M target fund, that meant $100K-$300K of personal capital. We didn’t have that. We’d need to bootstrap it through management fee deferrals and side arrangements.

Management fee: The standard 2% management fee on a $10M fund generates $200K per year. Sounds manageable until you realize that covers salaries, office, legal, travel, fund administration, and everything else. For two GPs, the math is brutal.

The GP business model realization:

Most people outside venture don’t understand this: fund management is a terrible business until you have multiple funds under management. The economics only work at scale. A single $10M fund generates enough management fee to survive, not thrive. Real GP wealth comes from carried interest—but that only materializes 7-10 years later, and only if performance is strong.

We modeled our GP business plan obsessively that quarter. The conclusion: we’d need to launch Fund II within 2-4 years to build a sustainable management company, and we’d need Fund I to perform well enough to attract larger commitments.

Building the LP Market Map with Asian Development Bank

One of the most valuable relationships we built during Year T-2 came through an introduction to Craig Dixon and Ian Lee at the Asian Development Bank (ADB).

ADB had been increasingly active in the South-East Asian venture ecosystem, not just as investors but as ecosystem builders. Craig and Ian were leading their emerging manager support program, and they agreed to spend time with us despite our lack of track record.

“We spent three intensive sessions with the ADB team building what we called our LP Market Map for South-East Asia,” I later explained at an AVCJ conference. “This wasn’t just a list of potential investors. It was a comprehensive mapping of LP types, their typical allocation patterns, their decision timelines, and crucially, their appetite for emerging managers.”

The LP Market Map revealed several critical insights:

• Most institutional LPs in the region had minimum check sizes of $5-10M, making them impractical for a $10M fund.

• Family offices and high-net-worth individuals were more accessible but required different approaches.

• Development finance institutions (DFIs) like ADB and IFC had specific mandates that we could potentially align with—but typically required larger fund sizes.

• Fund-of-funds focused on emerging managers were starting to look at South-East Asia but had limited presence.

• Angel networks and HNWI communities across Malaysia, Singapore, and Indonesia represented our most likely Fund I LP base.

July-September: LP Research and the Persona Problem

This was the quarter where we learned the most painful lesson of emerging manager life: LPs are incredibly difficult to understand, categorize, and access.

The LP universe is vast and fragmented:

Family offices (thousands of them across Asia, all different), pension funds (long decision cycles, high minimum commitments), fund-of-funds (professional allocators, very competitive), sovereign wealth funds (policy objectives, bureaucracy), corporate venture arms (strategic agendas), government programs (economic development mandates), endowments and foundations (mission alignment required), and high-net-worth individuals (relationship-driven, inconsistent).

We made every rookie mistake:

We built a target list of 550 LPs without understanding that 430 of them would never invest in a first-time $10M fund. We sent cold emails with our deck attached (never do this). We requested meetings without warm introductions (rarely works). We pitched our strategy without first understanding what each LP was looking for.

The LP persona problem:

Here’s what nobody tells emerging managers: LP motivations are incredibly diverse, and you can’t pitch the same way to all of them.

A family office investing generational wealth wants something completely different from a fund-of-funds managing institutional capital. A government development agency optimizing for economic impact has different priorities than a pension fund optimizing for risk-adjusted returns.

We wasted three months pitching features instead of benefits, strategy instead of fit.

The breakthrough moment came in August:

An experienced fund advisor told us: “Stop trying to convince LPs your fund is good. Start trying to understand which LPs your fund is good for. Ask yourself. ‘how are our customers? And why would they care?”

That shift changed everything.

We went back to our LP research and re-categorized everyone based on their likely priorities:

• Return-maximizers: Need top-quartile potential, accept higher risk, want concentrated portfolios

• Diversifiers: Want exposure to South-East Asian tech, acceptable returns, lower risk tolerance

• Strategic allocators: Have specific theses about sectors or geographies, want alignment

• Relationship investors: Invest based on people first, strategy second, need deep trust

• Mission-aligned: Prioritize impact alongside returns, want ESG integration

• Access-seekers: Want deal flow visibility, co-investment rights, portfolio company access

This framework helped us prioritize and customize. We stopped mass-pitching and started targeted outreach.

The Strategy Tools LP AI Platform: Practice Before the Real Thing

During this period, we discovered the Strategy Tools LP AI platform—a tool that allowed us to practice pitching to different LP personas before meeting them in real life.

“We found this immensely helpful,” Rizal recalled. “The platform let us practice nailing LP personas and value propositions pre-launch. We could simulate a conversation with a skeptical family office patriarch, a process-driven fund-of-funds, or a mission-focused DFI—and get feedback on how to improve our pitch for each.”

We ran through dozens of simulated LP conversations, refining our answers to the tough questions:

• “Why should we trust first-time managers?”

• “How will you compete against established Singapore funds?”

• “What happens if you don’t raise enough capital?”

• “Why Malaysia as your base?”

• “What’s your edge in deal flow?”

October-December: First LP Meetings and Brutal Feedback

By October, we had our legal structure in place, our deck polished (we thought), and our target list refined. We started taking meetings.

The first twenty LP meetings were a massacre:

“Your track record is insufficient.” (We knew this, but hearing it repeatedly was demoralizing.)

“Your fund is too small for our minimum commitment.” ($2M minimums into a $10M fund don’t work.)

“We’re not looking at emerging managers this cycle.” (Then why did you take the meeting?)

“Your thesis sounds like every other generalist fund.” (Ouch. They weren’t wrong.)

“Come back when you have a few investments to show us.” (The classic chicken-and-egg problem.)

Grace Choo’s perspective:

“I remember meeting Aisha and Rizal for the first time in late 2018. They were clearly smart, clearly passionate, and clearly unprepared for LP diligence. Their deck was too long. Their financial projections were too optimistic. They couldn’t articulate their differentiation in under sixty seconds. But what I did see was founder-quality determination. They took our feedback seriously. When they came back three months later, the improvement was dramatic. That’s the signal I would later invest behind—not perfection, but trajectory. Of course, fund I was not a good fit for us, but these conversations did lead us into fund II a few years later.”

December reality check:

By year-end, we had met with 93 potential LPs. We had zero commitments. Not soft commitments, not verbal interest—zero. Our personal savings were running low. Rizal’s wife was expecting their first child. I had stopped paying myself entirely, living off credit cards.

We had a hard conversation that Christmas: do we continue, or do we accept that this isn’t working?

We decided to give it six more months—but we needed to change our approach fundamentally.

The Cash Flow Reality: Surviving Pre-First Close

Here’s the dirty secret of emerging manager life that nobody talks about enough: you need working capital to operate before your management company generates fee income.

Our cash flow situation in Year T-2 was brutal:

Expense Category Amount

Legal fees for fund formation: $25,000

Travel to LP meetings and conferences: $15,000

Basic operations: $18,000

Deferred salaries (we weren’t paying ourselves): $0

Total pre-revenue burn ~$58,000

We funded this through personal savings, a small loan from Rizal’s uncle, and increasingly uncomfortable credit card debt. I stopped paying myself entirely. Rizal worked a consulting gig on the side to keep his family afloat.

This is the part of fund formation that the glossy conference panels never discuss. The reality is that most emerging managers in South-East Asia are living on the edge of financial viability until first close—and many give up before they get there. The 75% failure rate for first-time GPs isn’t because they have bad strategies. It’s because they run out of money and willpower before the strategy can be proven.

Year 0: The Long Road to First Close

January-March: Repositioning and Re-engagement

The first quarter of Year T-1 was about radical honesty.

What wasn’t working:

Our pitch was generic. Our main deck was too long (28 slides—should have been 12). Our answer to “why you?” was unconvincing. Our LP targeting was scattershot. Our follow-up was inconsistent. We did not use our LP CRM well enough. We were not disciplined. We had nothing about LP value propositions. We only discovered that part later.

What we changed:

We rebuilt our deck from scratch, focused on three things: team credibility, differentiated thesis, and LP value proposition. We cut everything else.

We developed specific LP personas with tailored pitch angles:

• For successfully exited founders in the region: Emphasized deal flow access and co-investment opportunities in the next generation of South-East Asian startups

• For active business angels: Emphasized portfolio diversification and professional fund management

• For HNWIs: Emphasized regional exposure and access to venture as an asset class

• For single family offices: Emphasized our accessibility, direct GP relationship, co-investment opportunities

• For angel networks: Emphasized our systematic approach to sourcing and supporting startups they could also access

We implemented a proper CRM (finally) and started tracking every LP interaction systematically. No excuses.

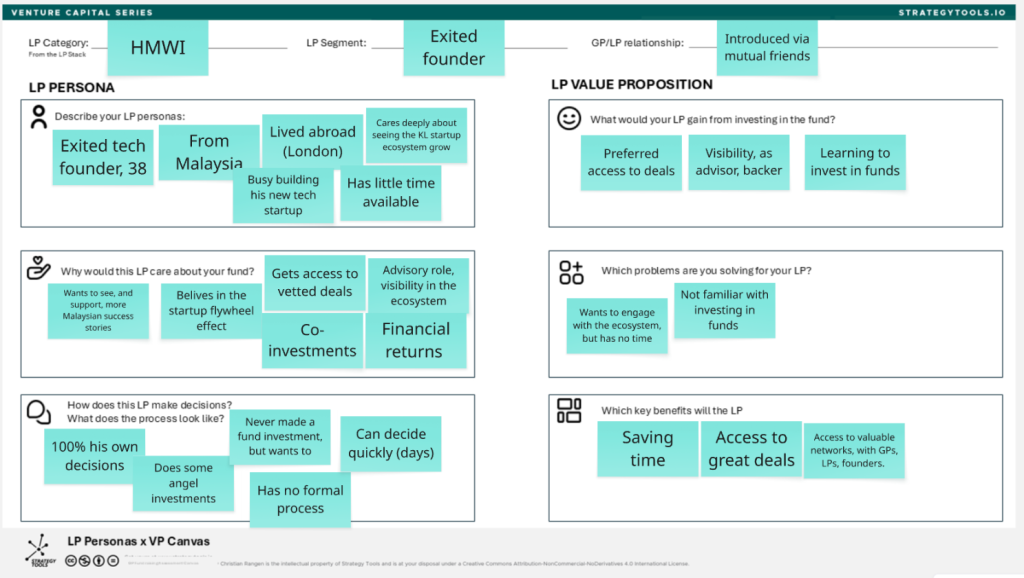

Using the LP personas x VP Canvas to nail the key message

Even more importantly, we started developing and iterating on the LP Personas x Value Proposition canvas for each of our LP personas, and for every LP we engaged with. It was awkward, slow even, in the beginning, but it helped us really tune into who are LPs were and what they cared about.

The breakthrough conversation:

In February, an LP we’d met six months earlier agreed to a second meeting. This time, they engaged differently. They asked about specific portfolio company scenarios. They probed our valuation discipline. They questioned our reserves strategy.

After ninety minutes, they said: “We’re interested in a $500K commitment if you can reach first close by June.”

Conditional, yes. But it was the first real signal of momentum.

April-June: Building LP Momentum

The domino effect:

That conditional commitment changed our LP conversations overnight. We went from “no one has committed yet” to “we have strong LP interest and expect first close within months.”

The power of anchor LPs:

We learned that LP fundraising has a herd dynamic. Once one credible LP commits, others become more comfortable. The first commitment is impossibly hard; the next ones are merely very hard.

In April, we secured a second conditional commitment from a Malaysian family office—$750K. In May, contributions from two angel networks indicated $1.2M combined. By June, we had verbal commitments totaling $4.5M.

The working capital problem resolved (barely):

We solved this inelegantly: Rizal took out a personal loan against his apartment. I maxed out my credit line. We deferred our own salaries entirely. It was financially precarious and emotionally exhausting.

Some emerging managers solve this through GP seeding programs or anchor LP arrangements that include working capital provisions. We didn’t have that luxury.

July-September: Legal Documentation Marathon

With LP momentum building, we entered the documentation phase.

LPA negotiations are brutal:

The Limited Partner Agreement (LPA) is the legal document that governs everything: fee structure, carry waterfall, GP removal provisions, key person clauses, investment restrictions, reporting requirements.

Every LP wanted changes to our draft LPA. Some wanted lower fees. Some wanted specific co-investment provisions. Some wanted side letters with enhanced reporting or most-favored-nation clauses.

We spent three months in legal negotiations that cost another $40,000 in attorney fees.

Key terms we fought for:

• Standard 2% management fee (some LPs pushed for step-downs)

• 20% carried interest with 8% hurdle and European waterfall

• 4-year investment period with possible 1-year extension

• 10-year fund life with two possible 1-year extensions

• Key person clause covering both Rizal and me

• GP commitment of 2% ($200K on a $10M fund—we’d figure out how to fund it through fee deferrals)

Key terms we conceded:

• Enhanced reporting to larger LPs (quarterly portfolio reviews, annual LP meetings)

• Co-investment rights for LPs on deals over $500K

• Advisory committee with LP representation

October-November: Racing to First Close

By October, we had $7M in executed subscription documents. Our target was $8M for first close, which would allow us to start investing with credibility.

The final push:

We called every warm LP relationship. We accelerated meetings with anyone showing interest. We offered modest fee concessions to LPs who could commit quickly.

The November crisis:

Three weeks before our target first close date, one of our committed LPs—an HNWI representing $1M of commitments—went silent. Emails unanswered. Calls unreturned.

After a week of panic, we learned through back channels that he was going through a divorce and had frozen all discretionary investments. Our $1M was gone.

We had two weeks to find $1M or miss first close. Missing first close would signal weakness to existing LPs and potentially trigger uncommit clauses.

The scramble:

Rizal flew to Hong Kong to meet face-to-face with a family office that had expressed interest months earlier but couldn’t meet our timing. I worked the phones, reaching out to every contact who’d ever shown warmth.

In the end, a successful entrepreneur we’d met at a Cradle Fund event committed $600K, and the Hong Kong family office committed $500K contingent on meeting Rizal in person (which he’d just done).

We made first close with $8.1M—not the $10M we wanted, but enough to start.

Year 1: First Close and First Investments

December-January: Operational Reality

First close on December 15th felt like victory. The relief was physical—I slept for fourteen hours straight.

But first close isn’t the end; it’s the beginning:

Capital calls went out. Management fee income started flowing, but we were still understaffed and under-resourced. Our $8.1M fund would generate roughly $162K in annual management fees. After legal, administration, office, and basic operating costs, we had enough to pay ourselves modest salaries—and nothing more.

The capital call mechanics:

We learned that fund accounting is surprisingly complex. Capital calls need to be calculated precisely, documented properly, and communicated to LPs with adequate notice. Our fund administrator handled most of this, but we still needed to understand it.

First capital call: $2M (roughly 25% of commitments), to be deployed over the first 12-18 months plus reserves.

The Friends, Family, and Angels Reality of Fund I

For Fund I, we failed at raising any institutional capital.

Every DFI we approached said our fund was too small. Every fund-of-funds said we lacked track record. Every pension fund said their minimums exceeded our entire fund size.

We had to pivot completely. Instead of institutional capital, we built Fund I from friends, family, high-net-worth individuals (HNWIs), angels, angel networks, and two local family offices.

Fund I Final LP Roster:

LP Type Commitment

Malaysian Family Office #1 $1.5M

Hong Kong Family Office $1M

Singapore HNWI (exited founder) $1.4M

AngelCentral Malaysia network $800K

Malaysian angel syndicate $700K

Various HNWIs (6 individuals) $2.7M

Friends & family $500K

GP Commitment (deferred) $200K

Fund I Total $10M (final close)

Final close at $10M came in March of Year 1, adding another $1.9M from additional HNWIs who saw our early momentum.

Fund I Economics: The Brutal Math

Let me share the fund economics of a $10M first fund, because this is where many emerging managers miscalculate:

Item Amount

Fund Size $10,000,000

Annual Management Fee (2%) $200,000

Fund Administration & Legal -$35,000

Office & Operations -$25,000

Travel & LP Relations -$20,000

Available for Salaries $120,000

$120,000 per year for two partners. That’s $60,000 each—less than entry-level roles at banks or corporations in KL, and far less than what we’d been earning in our previous roles.

The economics only work at scale. A single $10M fund generates enough management fee to survive, not thrive. Real GP wealth comes from carried interest—but that only materializes 7-12 years later, and only if performance is strong. This is why we knew from day one that Fund I was just the foundation. We would need to launch Fund II within 2-4 years to build a sustainable management company.

February-June: First Investments

Investment #1: DataSync (April, Year 1)

B2B analytics software for SMEs. Two founders from Grab’s data team. Pre-product, but extraordinary clarity on the problem they were solving. We led a $600K seed round, investing $400K.

Making that first investment decision was terrifying. Every doubt I’d had during fundraising resurfaced: Are we really qualified to make this call? What if we’re wrong? What if we’re just two people who convinced some LPs to trust us and now we’re about to deploy their capital into a company that fails?

Rizal talked me off the ledge. “We did the work. We believe in the founders. We understand the market. This is literally what we raised money to do.”

He was right. We wired the money.

Investment #2: PayMalaysia (May, Year 1)

Payments infrastructure for Malaysian marketplaces. Solo founder, ex-Maybank digital banking lead. Slightly further along—had a working product and three pilot customers. We lead an $800K round alongside an angel syndicate, investing $350K.

June 30 position:

Two investments deployed. $750K invested out of $10M committed. Management fee covering operations. Team of two GPs plus one part-time analyst. We were officially in business.

July-December: Continuing Portfolio Build

Investment #3: CloudSEA (August, Year 1) — SaaS for regional SME operations. Three-person founding team from enterprise software backgrounds. Early revenue, strong NPS. We invested $500K to lead a $1M round.

Investment #4: SecureKL (October, Year 1) — Cybersecurity for Malaysian enterprises. Deep tech founding team from local universities. Pre-revenue but compelling technology. We invested $300K in a $600K round.

Investment #5: LogiTech Asia (November, Year 1) — Last-mile logistics optimization for e-commerce. Solo founder, former Lazada operations manager. Pilot agreements with two major retailers. We invested $400K to lead her seed round.

Year 1 Portfolio Snapshot:

Company Investment

Status DataSync $400K Building product, pre-revenue

PayMalaysia $350K Growing, 5 customers

CloudSEA $500K Early revenue, expanding

SecureKL $300K Pre-revenue, developing

LogiTech Asia $400K Pilot stage

Total Deployed $1.95M 19.5% of fund

Year 1 Summary

By December 31 of Year 1, we had:

• $10M in committed capital across 14 LPs

• 5 investments made, totaling $1.95M deployed

• A functioning (if lean) operation with 2.5 team members

• Management fee income covering basic expenses

• Survived

We hadn’t thrived. We were chronically under-resourced. Our LP reporting was messy. Our portfolio support was reactive rather than proactive. I was working 70-hour weeks and still falling behind.

But we had survived. And in the emerging manager game, survival is the first milestone.

Key Takeaways from Part I

For aspiring fund managers:

1. The timeline is longer than you think. Budget 2-4 years from concept to first close. We took nearly 3 years.

2. LP fundraising is its own skill set. Experience investing or operating doesn’t translate directly. Study LP motivations obsessively.

3. Work backwards from GP economics. Understand what fund size you need to build a sustainable management company. Too small = you starve. Too large for an emerging manager = you don’t close.

4. Conditional commitments unlock momentum. One credible LP commitment changes every subsequent conversation. Prioritize getting that first anchor.

5. Working capital is existential. Have a plan for how you’ll fund operations before management fees flow. This is the most common emerging manager failure point.

6. Legal costs are real. Budget $75K+ for fund formation in South-East Asia. It’s unavoidable.

7. First close isn’t final close. Keep fundraising momentum through the investment period.

Grace Choo’s final perspective on Part I:

“Aisha and Rizal nearly quit three times during their fundraising journey. I know because they told me later, after Fund I was performing well. What they didn’t realize at the time was that their struggle was evidence of their commitment, not evidence of failure. Every emerging manager I’ve backed has had moments where they questioned whether it was worth it. The ones who break through are the ones who find a way to keep going. The Fund Journey Map shows this path clearly—but living it is another matter entirely.”

Ready for part II and III? Follow Aisha and Rizal’s journey into year 2,3 and beyond.

Read part II here and part III here.