From Fund I to Fund III Aisha and Rizal navigate nearly a decode on the fund journey. For Fund III, they run into the LP Outcome Canvas at one of Malaysia’s leading pension funds. (case based, fictional fund)

Read the full story, The Fund Journey: An Emerging Manager’s Story from Kuala Lumpur to South-East Asia, Part I (years T-2 -1), Part II (years 2-5) and Part III (years 6-7).

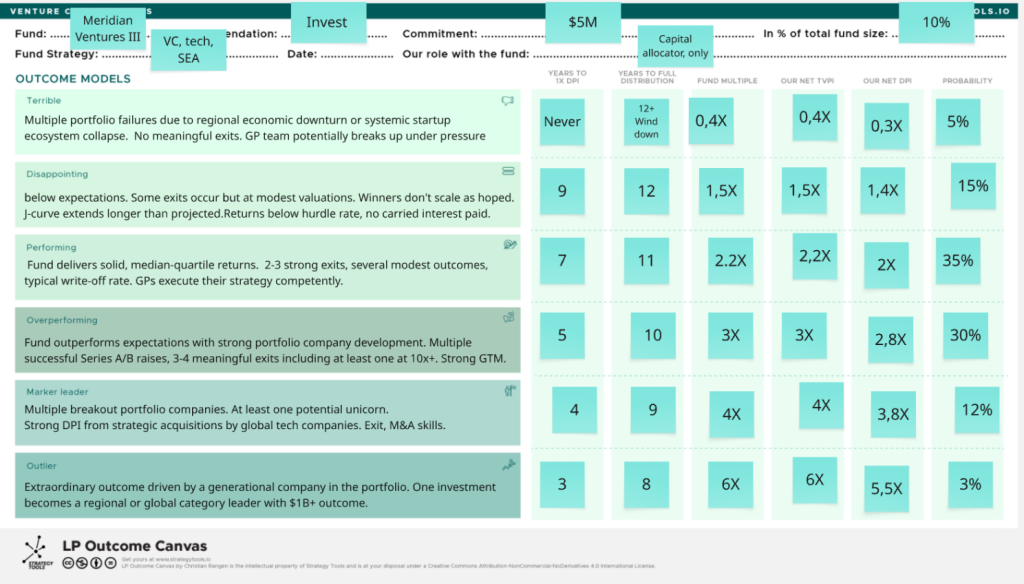

Fund: Meridian Ventures Fund III Fund Strategy: Early-stage B2B software, AI and fintech across South-East Asia (Malaysia, Indonesia, Vietnam, Philippines) Recommendation: Invest Date: October 5th

Commitment: $5,000,000 In % of total fund size: 10% Our role with the fund: Limited Partner with Advisory Committee seat

Investment Context

Employees Pension Fund (EPF/KWSP) is evaluating a $5M commitment to Meridian Ventures Fund III as part of our emerging manager allocation within the alternative investments portfolio. This represents our first commitment to Meridian, though we have tracked the firm since Fund II.

Why Meridian Fund III:

- Malaysian-based GP aligns with our mandate to support domestic asset managers

- Strong Fund I performance (2.8x TVPI, 0.6x DPI at Year 5)

- IFC co-investment provides institutional validation

- Proven team stability through challenging early years

- Clear thesis in B2B/fintech aligned with Malaysia’s digital economy priorities

Our Due Diligence Findings:

- GP team demonstrates resilience and discipline (DataSync write-off handled well)

- Differentiated GTM value-add through Venture Partner

- Conservative fund sizing relative to opportunity

- Strong LP re-up rates from Fund I/II (>80%)

- Institutional-grade reporting and governance already in place

Analyzing Fund III with the LP Outcome Canvas

Outcome Models

1. Terrible

Scenario Description: Multiple portfolio failures due to regional economic downturn or systemic startup ecosystem collapse. Fund deploys capital but majority of companies fail to reach Series A. No meaningful exits. GP team potentially breaks up under pressure.

What would cause this:

- Severe regional recession impacting startup funding environment

- Key GP departure (key person event)

- Systematic misjudgment in investment selection

- Follow-on funding market collapse preventing portfolio companies from scaling

Metric Value

Years to 1x DPI Never

Years to Full Distribution 12+ (wind-down)

Fund Multiple 0.4x

Our Net TVPI0.4x

Our Net DPI 0.3x

Probability 5%

Our outcome: $5M invested → ~$1.5M returned over 12 years. Significant loss but limited to committed capital.

2. Disappointing

Scenario Description: Fund performs below expectations. Some exits occur but at modest valuations. Winners don’t scale as hoped. J-curve extends longer than projected. Returns below hurdle rate, no carried interest paid.

What would cause this:

- Mediocre portfolio company performance across the board

- Regional exit market remains challenging (limited strategic acquirer appetite)

- Fund I outperformance was partially luck, not fully repeatable

- Competition from larger funds compresses Meridian’s deal access

Metric Value

Years to 1x DPI Year 9

Years to Full Distribution 12

Fund Multiple 1.5x

Our Net TVPI 1.5x

Our Net DPI 1.4x

Probability 15%

Our outcome: $5M invested → ~$7M returned over 12 years. Positive but below our target returns for venture allocation. Opportunity cost versus other alternatives.

3. Performing

Scenario Description: Fund delivers solid, median-quartile returns. Portfolio construction works as planned with expected winner/loser distribution. 2-3 strong exits, several modest outcomes, typical write-off rate. GPs execute their strategy competently.

What would cause this:

- Normal portfolio distribution: 20% winners, 50% modest outcomes, 30% failures

- Regional exit environment functions adequately

- Fund I success was real but Fund III faces more competition at larger size

- Team executes well but without breakout positions

Metric Value

Years to 1x DPI Year 7

Years to Full Distribution 11

Fund Multiple 2.2x

Our Net TVPI 2.2x

Our Net DPI 2.0x

Probability 35%

Our outcome: $5M invested → ~$10M returned over 11 years. Meets our baseline expectations for emerging manager venture allocation. Acceptable risk-adjusted return.

4. Overperforming

Scenario Description: Fund outperforms expectations with strong portfolio company development. Multiple successful Series A/B raises, 3-4 meaningful exits including at least one at 10x+. DPI generation ahead of schedule. Clear Fund IV momentum.

What would cause this:

- GTM value-add genuinely accelerates portfolio company growth

- 1-2 portfolio companies achieve regional leadership positions

- Favorable exit environment with active strategic acquirers

- Strong follow-on investor interest validates portfolio quality

- Team cohesion and capability continues to strengthen

Metric Value

Years to 1x DPI Year 5

Years to Full Distribution 10

Fund Multiple 3.0x

Our Net TVPI 3.0x

Our Net DPI 2.8x

Probability 30%

Our outcome: $5M invested → ~$14M returned over 10 years. Strong performance justifying emerging manager risk. Would support increased allocation to Fund IV.

5. Market Leader

Scenario Description: Fund establishes Meridian as the definitive early-stage firm in ASEAN ex-Singapore. Multiple breakout portfolio companies. At least one potential unicorn. Strong DPI from strategic acquisitions by global tech companies. Fund III becomes a reference point for regional emerging manager success.

What would cause this:

- 1-2 portfolio companies scale to $100M+ valuations

- Major strategic exits (Google, Microsoft, Grab, Sea acquiring portfolio companies)

- Meridian brand becomes synonymous with quality SEA early-stage deals

- Fund I fully distributed at 3.5x+, validating long-term track record

- Strong global LP interest in Fund IV at $100M+

Metric Value

Years to 1x DPI Year 4

Years to Full Distribution 9

Fund Multiple 4.0x

Our Net TVPI 4.0x

Our Net DPI 3.8x

Probability 12%

Our outcome: $5M invested → ~$19M returned over 9 years. Exceptional returns. Strong relationship for preferred access to future funds. Case study for our emerging manager program.

6. Outlier

Scenario Description: Extraordinary outcome driven by a generational company in the portfolio. One investment becomes a regional or global category leader with $1B+ outcome. Fund returns driven primarily by single massive winner, similar to early Sequoia or a]16z funds with breakout companies.

What would cause this:

- Portfolio company becomes the “Grab” or “Sea” of its category

- IPO or $500M+ acquisition of lead position

- Timing alignment with massive market expansion (e.g., regional fintech infrastructure buildout)

- Everything goes right for one extraordinary founder

Metric Value

Years to 1x DPI Year 3

Years to Full Distribution 8

Fund Multiple 6.0x+

Our Net TVPI 6.0x+

Our Net DPI 5.5x+

Probability 3%

Our outcome: $5M invested → ~$27.5M+ returned over 8 years. Transformational return. Would significantly impact our alternatives portfolio performance. Extremely rare but possible given early-stage venture dynamics.

Summary Analysis

Probability-Weighted Expected Outcome

Scenario Probability Fund Multiple Weighted Multiple

Terrible 5% 0.4x 0.02x

Disappointing 15% 1.5x 0.23x

Performing 35% 2.2x 0.77x

Overperforming 30% 3.0x 0.90x

Market Leader 12% 4.0x 0.48x

Outlier 3% 6.0x 0.18x

Expected Value 100% — 2.58x

Probability-weighted expected return: 2.58x net multiple on our $5M commitment

Expected dollar return: ~$12.9M over 10-year average holding period

Risk Assessment

Downside Risk (Terrible + Disappointing scenarios): 20% probability of returns below 1.5x

Base Case (Performing): 35% probability of solid 2.2x returns meeting our venture allocation targets

Upside Potential (Overperforming + Market Leader + Outlier): 45% probability of 3.0x+ returns

Risk/Reward Assessment: Asymmetric return profile typical of venture capital. Limited downside (maximum loss = committed capital), significant upside potential. 45% probability of strong outperformance justifies the allocation.

Recommendation

INVEST $5,000,000 in Meridian Ventures Fund III

Rationale:

1. Expected returns justify risk: 2.58x probability-weighted return exceeds our 2.0x threshold for emerging manager venture allocations.

2. Downside is bounded: Even in terrible scenario, loss limited to committed capital. 80% probability of returning at least 1.5x.

3. Strategic alignment: Malaysian-domiciled GP supports our mandate. B2B/fintech thesis aligns with national digital economy priorities.

4. Institutional validation: IFC’s $8M commitment provides comfort on GP quality and governance standards.

5. Relationship value: Establishing relationship now provides access to Fund IV at larger scale if Fund III performs.

6. Portfolio fit: $5M commitment represents appropriate sizing for emerging manager allocation—meaningful enough to matter, small enough to absorb potential loss.

Conditions:

- Advisory Committee seat to maintain visibility into fund operations

- Quarterly reporting at institutional standards (already confirmed)

- Co-investment rights on deals above $2M (standard LP terms)

- MFN on any preferential terms granted to other LPs

LP Outcome Canvas by Strategy Tools. Get yours at www.strategytools.io

Read the full story, The Fund Journey: An Emerging Manager’s Story from Kuala Lumpur to South-East Asia, Part I (years T-2 -1), Part II (years 2-5) and Part III (years 6-7).

About the Author:

Christian Rangen is a strategy advisor and business school faculty. He works with ambitious ecosystem developers, innovation agencies, venture funds, national fund-of-funds and governments on building better VC firms and VC ecosystems. He runs GP Accelerators and GP Masterclasses globally.